India’s presidency must leave the grouping with the agility and energy to respond to new realities, and it must create a future-ready multilateralism through a novel and robust institutional architecture

India takes over the presidency of the group in December. To live up to the potential of this opportunity, it must choose a policy direction to focus on continuity, incorporate green and digital transitions, and recognise the realities of a post-pandemic world

India’s presidency of the G20 grouping next year — arguably the sole remaining effective forum for global governance — presents an enormous opportunity to accelerate sustainable growth within India, in the emerging world, and beyond.

For India’s presidency to live up to this potential, it must recognise the constraints of the grouping and the crises — from the pandemic to the Ukraine war — that it must confront. But there should also be a clear understanding of the levers that a G20 president has to affect global policy action.

Next year, the troika of the preceding, current, and succeeding presidents will be three developing countries: Indonesia, India, and Brazil. This fortuitous alignment must inform India’s strategy as it designs its G20 agenda.

Three broad principles should underline India’s planning. First, it must recognise the value of the emerging-world troika and choose policy directions that emphasise continuity. Second, it must incorporate the concerns of its dual development transitions — green and digital — into the G20’s agenda. And third, it must recognise the realities of the post-pandemic world and prioritise action on those sectors that have, since 2020, been revealed to be under-capitalised.

India’s agenda must resonate beyond the one year it holds the presidency. This requires it to set its priorities alongside those of the two other members of the troika. The G20 under Indonesia has articulated three priority issues — global health architecture, digital transformation, and sustainable energy transition. Reinterpreting these will be key to building continuity, and, thus, sustained action. It is also important to keep in mind that having too many priorities is the same as having none at all. Indeed, India must prevent the G20 from suffering — as other multilateral forums such as the World Trade Organization do — from an over-expansion of its mandate.

Two major transformations will define our economies and societies going forward: Digital transition and green transition. Both are key to addressing the development challenge as well. These transitions are the meeting point of geopolitical and youth aspirations that will dictate our political, economic and social well-being.

On the digital front, India, to a large extent, has been a first mover. India’s youth aspirations are digital-first; the government has responded, and the digital economy is at the centre of its aim for a $5-trillion economy by the second half of the 2020s. The Observer Research Foundation’s youth survey on tech policy found that 83% of respondents want India to adopt a policy that prioritises its domestic technology industry. At the same time, 80% welcome greater cooperation with international partners on technology.

Clearly, a fine balance is needed where technological multilateralism does not come at the cost of developing countries’ needs. The Think Tank 20 (T20) engagement process has identified the internet as a basic right and technology access as vital to reducing inequalities. Cooperation at the G20 would be a good testing ground for pioneering tech regulation that balances the interests of the private sector with sovereignty and the security needs of States, and the growth demands of the economy.

India’s G20 must also recognise the unprecedented, carbon-constrained nature of future growth. Arguments for a green transition can no longer be limited to the moral high ground of saving the planet. A commitment on sustainable consumption must be placed front and centre. International financial regulation and the mandates of multilateral development banks must also ensure that adequate finance incentivises a business case for rapid change with adequate global flows subpoenaed for the developing world. Can the Indian presidency help to architect this new global arrangement?

A third focus must necessarily be the post-pandemic world order. Covid-19 has proved that health, nutrition, and livelihoods all remain fragile despite commitments made under Agenda 2030. The United Nations has warned that the Covid crisis could result in a lost decade for development. It has sharpened inequalities and widened development gaps. The United Nations International Children’s Emergency Fund has also cautioned that the pandemic could lead to a “lost generation” of children in terms of education, nutrition, and overall well-being. These conversations have become more complex due to the crisis in Ukraine. The weaponisation of trade and the international banking system during this war has exacerbated uncertainties. The surge in prices of energy and essential staple foods has added a disturbing dimension to an already stressed economic recovery. By putting nutrition, food security, and health at the heart of its G20 agenda, India can ensure the success of the Decade of Action on Sustainable Development. The clincher will be to facilitate greater funding towards these efforts.

India’s presidency is an opportunity to reinvigorate, reinvent and re-centre the multilateral order. The G20 cannot be distracted or undermined by the bilateral relations of specific members, even as we acknowledge the gravity of the humanitarian crisis that is unfolding in Europe. India must leave the G20 with the agility and energy to respond to new realities, and it must create a future-ready multilateralism through a novel and robust institutional architecture.

Our text of ancient fables, the Panchatantra, speaks of “natural allies”. If there are ever natural allies in politics, the European Union (EU) and India should exemplify this relationship. Our cultural exchanges date back to ancient times; our languages have common roots; our borders are closer than ever via a human bridge that connects us: There are millions of Indians in the Middle East, and millions from the Middle East in Europe. Europe and India are a geographical continuum. And both the EU and India— “the world’s largest democracies”—face shared threats and challenges. All roads must now connect Delhi and Brussels.

Here, we lay out a map to address three key challenges: The green transition, the digital transformation, and the preservation of our shared geopolitical landscape. On all three issues, direct and close cooperation between the EU and India will not only be vital for these two major powers and their people—but also for the world at large.

Green Transition

To address climate change, the EU and its members have been upping their domestic game. The European Green Deal is only one amongst several key initiatives that illustrate the seriousness with which the EU is addressing the existential threat of climate change. At the same time, there is much angst in Europe that these efforts will not suffice unless they are matched by China and India. While the concerns are understandable, a narrative framed in terms of “what will become of the world if every Indian has a car” is patronising and misplaced, especially when one compares the per capita fossil consumption in India to the EU members. In any case, specifically with respect to India, the EU is pushing through an open door on the issue of addressing climate change. India has led the way in international initiatives on the issue of clean energy, for instance, by creating the International Solar Alliance with France. India’s commitment to protecting the environment, moreover, does not stem from recent pressure exercised by Greta Thunberg or Fridays for Future. Contra western anthropocentrism in which activists advocate climate change mitigation for “our children’s future”, Indian philosophy teaches us that the planet belongs to humans, plants, animals, and all living beings. There are, therefore, deep-rooted and inclusive reasons for Indians to be committed to protecting the planet. This commitment should not be doubted. Instead, the EU needs to find ways to invest in this Indian cause and co-create solutions for our common future.

The European Green Deal is only one amongst several key initiatives that illustrate the seriousness with which the EU is addressing the existential threat of climate change.

To achieve this, we need actions and not words. It has taken a full-blown war in the heart of Europe for Germany to recognise the risks of over-dependence on Russia for energy purposes; diversification is proving to be far slower and more complicated than many would like. In light of this experience, it is perhaps even more unreasonable than before to demand that India “phase out” coal at the click of a finger. The EU will have to put its money where its mouth is if it is serious about addressing the global problem of climate change. The Carbon Border Adjustment Mechanism, for example, should be more than a “poverty tax”, as it is seen in India; it should be a tool to finance and incentivise the green transition in globally integrated sectors in the emerging world. Technologies vital to low-carbon growth will need to be co-created and co-owned by Europe and partners like India. European capital must be given a nudge to flow into climate-conscious investment in the emerging world. It is up to the EU to make sure that India’s efforts pay off—through significant European financing in key sectors, via public-private partnerships.

Digital Transformation

The EU is leading the way in setting people-centred standards on digital governance via GDPR. India’s Aadhaar Card scheme has shown the pioneering role that digitalisation can play in empowering the poor and facilitating development. There are also already several worrying examples of the pernicious effects of digital technology: Surveillance of local populations by authoritarian states, as well as the manipulation and control of infrastructure and security systems by external actors. To preserve the individual liberties of their people, and strengthen digital sovereignty, European and Indian cooperation will be key.

Research collaborations on dual-use technology, public-private partnerships for implementation and marketing of these innovations, and working jointly and through like-minded coalitions to establish rules for data governance and cyber-security are essential.

These two democratic powers will also be well-served to collaborate on diversifying away from their dependence on China, for e.g., on 5G technology and infrastructure development. Any trade agreement between the EU and India should prioritise this key consideration. Research collaborations on dual-use technology, public-private partnerships for implementation and marketing of these innovations, and working jointly and through like-minded coalitions to establish rules for data governance and cyber-security are essential. Neither the EU nor India can get left behind in a game that is dominated by the boardrooms in the US and party headquarters in China. India and the EU need to enter into a technology partnership that allows for all of this, and for ensuring reliable and integrated supply chains.

Shared geopolitical landscape

Our shared geopolitical landscape—extending beyond geographical proximities and including the Indo-Pacific—has been under extreme stress in recent years. The EU has a war triggered by Russia on its borders; India and its neighbours have had to put up with Chinese adventurism on the Himalayas and in their maritime neighbourhood.

Research collaborations on dual-use technology, public-private partnerships for implementation and marketing of these innovations, and working jointly and through like-minded coalitions to establish rules for data governance and cyber-security are essential.

This is a time for both the EU and India to be working together to help restore balance in the region. The EU will need to jump off the fence with respect to China; the European mantra of “partner, competitor, rival” is highly inadequate in dealing with a China that has signed a “no-limits” partnership with Russia. India will also need to rethink its own dependencies. The two democracies have now very real incentives to develop closer economic and military ties.

Sanctimonious lectures about morality will need to be replaced by a shared empathy of the like-minded. And all this will require the use of not only Europe’s favourite tool of “soft power”, but also the use of hard power through infrastructure projects, green investment, and military cooperation. Re-aligning their economic and security cooperation with each other will enable both the EU and India to stand up for the values that they both hold dear: Democracy and pluralism.

As the price of natural gas reached record highs in the UK and Europe—trading at the equivalent of $200 per barrel of oil,[1] and as economic activity in China has been curtailed by the country’s power supply crunch, central bankers and policymakers from across the globe are forced to confront significant challenges to price stability, with a focus on shielding households and businesses from an increase to the cost of transport and basic goods, while monitoring the potential for price pressure and supply chain bottlenecks to upend the global economic recovery. This is important at this time, for the ripple effects of disruptions to energy markets could amplify social and political fissures that are visible across the global landscape, and which might portend complex domestic politics as many countries head into elections in 2022.

Surging demand for natural gas—and shortages and bottlenecks to supply—have resulted in a corollary demand for oil products (referred to as gas-to-oil switching), thus driving up the price of WTI crude to seven-year highs.[2] The skyrocketing commodity price environment has led one observer to point to the “revenge of the old economy”, according to which the collective noble efforts to move toward a cleaner, greener future fuelled by renewable energy have been stymied by a recent past of inadequate investment into the capacity and infrastructure of the hydrocarbons that power our economies.[3]

Thus, even as COP26 has drawn to a close, and as policymakers, business leaders, and investors have left Glasgow with firm commitments to ostensibly advance the decarbonisation agenda, we are reminded of the extent to which our entire energy infrastructure still hinges upon the use of fossil fuels. This includes oil used for transport or power generation, or natural gas (or coal) for power generation, as well as natural gas deployed as “bridge fuel” to support the growth of renewable energy, including wind, solar, and hydrogen. This is effectively captured by what transpired in Germany earlier this year. In the first six months of 2021, the country increased its coal-based generation, which contributed 27 percent of the country’s electricity demand.[4] The need to resort to coal-fired power generation is not unique to the case of Germany: the US has also posted the first annual increase in coal use for power generation since 2014.[1] The combination of an asynchronous economic recovery, attendant shocks to demand, curtailments of supply, and surging prices in natural gas are contributing factors to rich income countries’ pivoting toward the use of coal. This illustrates one stark reality: hydrocarbons continue to underpin our global energy infrastructure.[5] For all the talk of “stranded assets” and potential “dinosaurs of investment”,[6] hydrocarbons still compose the lion’s share of energy consumption on a global basis.[7]

What are the lessons to be learned from the recent power crunches? And what are the potential macro, socio-economic, and geopolitical implications as we navigate the energy transition? Amidst so much uncertainty and volatility, where are the opportunities for accord, as well as bright spots for investment?

Humility is also requisite as governments confront their energy interdependence with one another: again, despite record growth in renewable energy capacity,[8] and surging climate financing, countries within the European Union are poignantly aware of their dependence upon natural gas imports—whether from Russia, Norway, or the US. And even despite its own domestic shale and conventional oil and gas production, the US continues to import hydrocarbons from countries such as Canada, Colombia, and Saudi Arabia. Similarly, even despite trade tensions, resource ties still bind China with Australia, with the latter having exported a record volume of natural gas to China in 2020.[9] Thus, geopolitics remains at the very heart of the changing energy landscape. The inverse is also entirely true.

In the past, resource ties have been a source of tension; but, as we shall see, such bonds also have the potential to become a geopolitical salve, provided that the relationship is designed to be mutually beneficial to both parties. As we navigate the path toward net zero, and by seeking balance and diversification, our continued energy interdependence can actually spur opportunities for cooperation amongst policymakers, and for long-term investment and profit generation for enterprises and economies around the world.

The quest for resources to fuel industrial growth, military campaigns, and transport and urbanisation lies at the very heart of geopolitics. In considering the relationship between energy and geopolitics, the existence of resources is often associated with tension, be it in the form of border disputes, armed conflict, trade disputes resulting in embargoes, or interstate conflict or war. Access to strategic reserves of coal in Romania was a pivotal part of the campaign on the Western front during the Second World War. During the 1970s, energy-importing countries experienced the oil shocks related to the OPEC crises in the wake of the Arab-Israeli War, the Yom Kippur War, and the Iranian Revolution.[10] Indeed, research shows that if a resource-rich country has an endowment of oil along its border with an “oil-less” country, then the probability of conflict between these two countries is higher than if there were no oil at all.[11] Recent data also indicates that the presence of onshore oil might even portend a higher rate of conflict than the presence of offshore oil, as the potential for production and output to be seized by rebel groups is far higher on land than it is in deep-sea projects.[12]

And yet, while asymmetric access to resources might spur tensions between countries, it can also be a geopolitical salve, by underpinning ties of trade, development, and civic diplomacy and even employment. Japan’s quest for resources to fuel its extraordinary manufacturing era from the 1960s onwards resulted in a mutual export of ODA (overseas development assistance) to southeast Asian countries such as Vietnam. One might also argue that Israel’s relatively recent discoveries of natural gas—and successive exports to Egypt—have also underpinned a normalisation of relations with Cairo, — a diplomatic rebalancing which has also been a key facet of improving relations between Israel and the UAE.

A crude awakening: our enduring energy interdependence, and continued reliance upon fossil fuels

Such positive examples of resource ties are swiftly forgotten in times of crises. The underlying conditions that led to positive benefits to the political relationship in these two instances are also ignored. And so it is with the present power crunches ricocheting across the globe. With the asynchronous reopenings of economies in the wake of the COVID-19 pandemic—and amidst ongoing disruptions to supply (be it from underinvestment in hydrocarbons, weather-related events such as flooding, pandemic-induced stoppages to production, or port congestion)— we are reminded not only the extent to which our economies depend upon fossil fuels for power generation and for transport, but also, of the extent to which many countries remain deeply interlinked in patterns of energy interdependence.

The European dilemma regarding natural gas supply from the Russian Federation is instructive, but it must also be recognised that energy interdependence cuts both ways. As long as Russian gas is a competitive source for energy, then energy-hungry European manufacturing powers will need to engage with the leadership in Moscow; equally, as long as Europe has access to alternative sources of fossil fuels – even if not as cheap – Russia will need to retain an understanding of European red lines. This is what interdependence means. This insight is equally applicable to the energy interconnections of the future: China can be a useful partner in the energy transition, even if it is not the only one.

Indeed, for some policymakers, part of the allure of developing domestic renewable energy capacity was that it ostensibly would lead toward more enhanced energy independence. Ostensibly, extraordinary efforts in diplomacy might not be needed in such a green future, as countries would, in theory, no longer be reliant upon conflict-ridden territories to secure energy supply. Even in a net-zero future, this is perhaps to view the world through rose-coloured glasses: for the development of wind, solar, and hydrogen energy—or indeed techniques of greater energy efficiency—at an affordable cost is intrinsically related with garnering supplies, inputs, R&D, and human capital from different jurisdictions. Overly halcyon scenario-planning for domestic renewable energy capacity development often fails to incorporate these facts.

The shift from fossil fuel-based to renewable energy capacity does not end interdependence; it merely pushes interdependence to a different part of the energy mix. The dependence now shifts from hydrocarbons to metals and from ores to rare earths. Countries in Africa, Asia, Americas and Australia are likely to emerge as global mineral hubs, and the routes to ship these new commodities might pave new geostrategic highways.

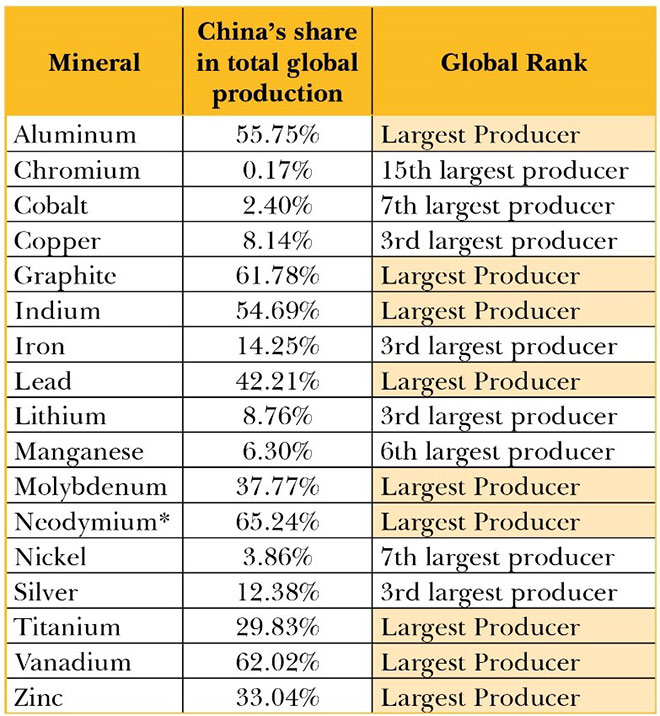

In recent years, control over the production of rare earths has become a familiar site for geopolitical tension. In 2021, the Biden administration in the United States ordered a review of the country’s critical mineral supply chain; the recommendations included prioritising development financing for “international investments in projects that will increase production capacity for critical products, including critical minerals”.[13] The administration’s concern is readily understandable, as shown in Table 1.

Table 1: China’s share in the rare earths supply chain

*Disaggregated data for neodymium was not available; the data for Rare Earth Concentrates (REO) has been used since neodymium is a rare earth metal.

Yet it is not just production of rare earths that will be relevant, but also the locations of their processing and other forms of value addition. These might emerge as the equivalent of present-day refineries and petroleum complexes, and their distribution potential linked to key consumption centres might lead to the birth of new geostrategic lynchpins such as the Straits of Malacca and of Hormuz. The notion that domestic renewable energy production would free countries from the intricacies of dependence is misguided – and a seminal mistake if it was to be the basis of new energy order.

Sunset on Malthus?

Part of the reason why the aspiration of energy independence retains its sheen is that our energy economics and policymaking continues to be suffused with a Malthusian legacy.[14] Said another way, the spectre of scarcity continues to inform the way we think about energy and resources. The fear that “there will never be enough” renders misgivings about dependence—or else outright denial. A sense of energy insecurity –no matter how much it is brushed under the rug might also prompt a premature and imprudent vaunt into a disorderly energy transition, with a disproportionate focus on bolstering capacity at home. Such a policy would have little regard for the fact that climate change has been branded as humanity’s largest negative externality: in order to mitigate the situation, global actions ought to be in concert. Humility is thus needed not only in recognising the endurance of hydrocarbons within the energy mix, but also, but it is also implicit in our interconnectedness as we navigate the green transition. For the rich income countries, part of this humility also requires understanding the various ways in which the energy transition has the potential to deepen the chasm between the ‘haves’ and the ‘have nots’.

The haves and the have-nots: is the energy transition deepening the chasm?

The energy transition has the potential to create a deeper chasm between the standings of the ‘haves’ and the ‘have nots’ in the global macroeconomic environment. First, if we consider the traditional trajectory of industrial growth—that is, from agrarian activity to textile production, and then from heavy industry to light manufacturing, eventually segueing to services-oriented economies—the case can be made that for developing countries earlier on the maturity curve (such as Vietnam and India), stringent measures toward decarbonisation might actually thwart what would otherwise unfold as a full evolution of robust domestic industry. For the ‘price takers’ and for commodity-hungry countries, this might take the shape of premature restrictions on access to or use of resources to fuel domestic manufacturing activity.

And for the ‘price makers’—that is, commodity-rich exporting countries—the case can also be made that swift or unrealistic moves toward decarbonisation might rob oil and gas exporters from a significant base of output as well as a source of gross national income. In a country in which resource wealth underpins GDP, export activity, employment (both directly related to exploration, extraction and production of natural resources, as well as indirectly, via civil service salaries), national income, and sovereign and pension funds, the potential for social fissures to either manifest or to be exacerbated is clear.

It should be noted that history indicates that access or proximity to natural resources is not perfectly correlated with a trajectory of sustainable economic growth—hence the “Dutch resource curse”. Research from Brazil also indicates that oil endowments within a province or a municipality do not necessarily result in improved livelihoods for members of that community.[15] Indeed, even in a lofty commodity price environment, such as at present, windfalls potentially reaped from higher export prices of oil and gas do not always translate into higher incomes for households within the exporting country.[16]

This tension between environmental and the development agendas within emerging markets and developed economies (EMDEs) is also evident in the debate surrounding the potential carbon border adjustment tax (CBAT), as well as recent agreements on deforestation in COP26.

Home game: mitigating the domestic bias of climate finance

An effective, secure energy transition is currently undermined by the “domestic preference” evident within the realm of climate finance. In recent years of tracking climate finance flows, data from one leading industry body evidences that 76 percent of capital is invested in the same country in which it is sourced.[17] Thus, despite various commitments and guarantees from bodies such as the G7 or the G20, a significant challenge remains regarding the ability for much-needed climate finance to cross borders.[18] Certainly, a long-running trend of a domestic bias for investment is not limited to climate and infrastructure investments. Rather, it extends across sectors and asset classes, including real estate, energy, private equity, and venture capital. Whilst managing ‘sticky capital’ and the prospect of generating long-term returns, and building up enterprise and asset values, investors might harbor an inclination to place their money close to home—in other words, “where home-country risks are well-understood.”[19]

As these authors have highlighted previously, playing close to home in infrastructure investing may not always be the least risky option.[20] And yet, we have already motioned that the dawning age of renewables is not one of energy independence, but of a new kind of interdependence. Policymakers operating under the illusion of energy sovereignty are otherwise missing out on the opportunity to cultivate positive structures of interdependence which could potentially support their own geo-strategic aims – such links, might, in turn, spur opportunities for private investment.

Thus, we might witness a shift in incentivisation for private finance and the climate problem: such that sticky capital not only supplies the domestic market, but that it is directed outwards as well, perhaps even towards the geographies where host countries of finance might find mutually beneficial resource ties – such as the model of Japan and ODA in Southeast Asia, discussed earlier. As argued above, interdependence can be a salve for geopolitics as long as both sides gain in the energy or in the development equation. Such a value exchange – or what Michael Oakeshott refers to as an “enterprise association” – rests upon an understanding of interdependence – again, something that has been jettisoned in the lack of humility in the energy transition (something which is mirrored in the “domestic bias” of climate capital).

Such misconceptions have the potential to divert policymakers from a future of true sustainability, which involves the creation of resilience through diversification. Redirecting long-term flows of investment—including private capital—towards emerging market/developing economies will not necessarily be easy. Large sources of private capital in the global north – whether institutional capital or banks – will need a fresh set of incentives to invest in the energy supply chains of the future.[21]

Moreover, recognising that these investments will likely be in new minerals, new processes, and new geographies, it is clear that old regulatory risk models may no longer be suitable. New market mechanisms to help enable a level playing field of investment in new energy materials are needed—which might take inspiration from the industry bodies which have developed over time in support of oil markets around the globe.

Conclusion: The Green Marshall Plan

The scale of the rebalancing required – of investment, attention, and financial flows – is vast. If anything, it should be compared to the Marshall Plan. That enormous effort, after all, had both pragmatic and idealistic motivations. On the one hand, it was necessary to assist a Europe devastated by war; on the other, it was essential that a liberal community be built that was strong and resilient in the face of the Soviet challenge. There are similar overlaps today between the realist search for security and the idealist requirements of climate action. A Green Marshall Plan has the potential to both stabilise international relations and create the diversification and resilience necessary to allow for durable interdependence during the energy transition.

For the energy transition to act as a geopolitical salve rather than as a source of discord, a Green Marshall Plan must have four characteristics.

First, it should be genuinely global in character. A global net-zero approach would understand that some regions might take longer on the fossil fuel transition because of the specifics of their development or their energy landscape. Nor should geographical factors be ignored: An archipelago like Indonesia will take longer to transition to solar energy and away from natural gas than a continental country.

Second, legacy energy infrastructure will need attention to help enable the success of the Green Marshall Plan, to make it implementable, and to scale it. As is evident in energy consumption patterns across the globe, fossil fuels remain a part of the energy mix, and a way of working toward a balanced and global green transition. Nor can sectors like mining be ignored: the Green Marshall Plan will likely have to go into a “dirty” sector, invest in new ways of mining and new materials to mine.

Third, the Green Marshall Plan is not just about blue-sky research into the possibilities of the future. It is about increasing investment in nuts-and-bolts manufacturing in underserved geographies as well – whether energy efficiency in the Asian steel producers of the future or new cobalt mining technologies in sub-Saharan Africa today. It is about enabling development of critical frontier technologies, as well as swiftly and sustainably spreading a green ‘know-how’ which is globally benchmarked.

And fourth, the Green Marshall Plan should embed energy resilience at its heart. Areas which have sped up their energy transition are those where it is seen as assisting in energy security. As these authors argued, dependence on a single source or vendor is antithetical to achieving long-term and sustainable energy security. As such, the strategic mapping of a secure energy future cannot exclude a China, with its strong presence in the rare earths supply chain, or a Russia with reserves of natural gas, or the countries of the Gulf, abundant in oil and gas reserves. Again, humility as well as diversification might render each actor a more responsible and empathetic participant in the global energy transition.

What we are recommending is an all-inclusive future. That will require the leaders of key nations to invest political capital in a new institutional framework that supports the energy landscape of the future. The International Energy Agency, OPEC, commodity exchanges and others defined and shaped the hydrocarbon world. The global energy transition requires new frameworks, organisations and political arrangements to underwrite our common journey ahead, which reflect the needs of multiple stakeholders, in both the private and public spheres. The G7’s B3W, the European Union’s Global Gateway, and the Indo-French International Solar Alliance all point to one imperative: of green arrangements underwriting green transitions. The world needs a new institutional structure: one that keeps the lights on in the 21st century.

[5] See also, Vivan Sharan and Samir Saran, “India’s Coal Transition: A Market Case for Decarbonisation,” ORF Issue Brief No. 505, November 2021, Observer Research Foundation.

[14] For an excellent discussion of how Malthus continues to cast a long shadow on economics in advanced economies, see J.K. Galbraith, The Affluent Society (US: Houghton Mifflin, 1958).

This article was first published in The Economic Times Magazine

The narrative of a widening strategic gap between New Delhi and Moscow has been prevalent for some time now. Even within the strategic communities of Russia and India, there is an ongoing assessment of the importance of this bilateral engagement. Ahead of the upcoming India-Russia summit, this article delves into what is working for the relationship between the two nations, and what needs to be worked on.

It would be fair to say that the essential glue keeping the two together is strategic legacy. It is supplemented by a contemporary strand of political convergence in a world where both South Block and the Kremlin are actors, but also being acted upon.

One of India’s primary objectives in the coming decades is to prevent China’s hegemony in Asia. A multipolar world and a multipolar Asia are in its interest. Russia will strongly endorse this, and, for differing reasons, seek it. In its calculus, it would position the US as the principal protagonist to thwart. The Russians would not want to curtail China if that ends up enabling US influence. Therefore, there is a big picture convergence on a multipolar world order, even as India and Russia differ on relative roles of the poles shaping this order.

As of 2020, Russian weapons systems and equipment accounted for about 60 per cent of the inventory of the Indian armed forces.

This could change dramatically if Russia were to reach the conclusion that it is happy to sit in the court of the Emperor in Beijing as a junior partner. India sees this as unlikely. It hopes for a more independent Russian worldview that would not hesitate to differ with others, including China, in defence of its own interests. New Delhi is, therefore, continuing to invest substantially in this relationship, and in a number of areas.

The first and biggest is defence. As of 2020, Russian weapons systems and equipment accounted for about 60 per cent of the inventory of the Indian armed forces. While India is determinedly diversifying sourcing of military hardware, Russia remains a strong legacy player. Much of this is driven by spares and component upgrades. However, there have also been significant new ventures. These include the S-400 missile contract (on track for first deliveries this year); manufacture and co-production of four Project 1135.6 Frigates; manufacture of the world’s most advanced assault rifle – the AK-203 – under the ‘Make in India’ initiative; and additional deliveries of T-90s, Sukhoi-30 MKI, MiG-29, MANGO ammunition and VSHORAD systems. Russia is more involved with the ‘Make in India’ initiative in defence equipment than any other country.

Simultaneously, exercises have also increased in numbers and sophistication. As he demitted office as Indian Ambassador in Russia, DB Venkatesh Varma pointed out that the two nations were exploring different formats – including mobilisation of forces and their transportation across long distances, impact of drone technology on modern warfare, and impact of cyber on future of conflict. The landscape for doctrinal coordination and understanding is ever expanding.

India aims to increase import of oil from Russia, currently 1 per cent of all imports, to 4 or 5 per cent in the next five years.

The second area of convergence is energy. This includes not only hydrocarbons (oil and gas), but also nuclear. While India does import gas from Russia, a rapid increase is on the cards. If successful, the Vostok negotiations will bring India into one of the world’s biggest energy projects. India aims to increase import of oil from Russia, currently 1 per cent of all imports, to 4 or 5 per cent in the next five years. Another avenue is petrochemicals, where a Russian investment in the Paradip cracker plant and an Indian investment in Arctic LNG-2 are being explored.

The third area of mutual interest is high-technology. A proposal to establish a Joint Commission on Science and Technology Cooperation is being explored. It would encompass hi-tech areas like quantum, nanotechnology, cyber, AI, robotics, space and bio-technology. Pharmaceuticals, digital finance, chemicals and ceramics are all potential economic drivers of the relationship. Each of these is at the core of the fourth industrial revolution.

The fourth area of significance is food security. India leasing land in the Russian Far East, and cultivating it with Indian labour, offers a tantalising prospect. Russia is going through a demographic crisis and has notable human resources deficits. China has leased thousands of hectares of land in the Russian Far East. This is cultivated by Chinese farmers, whose produce is partially sold in the Russian domestic market and partially exported to China.

A proposal to establish a Joint Commission on Science and Technology Cooperation is being explored. It would encompass hi-tech areas like quantum, nanotechnology, cyber, AI, robotics, space and bio-technology.

A similar strategy can be followed by India. The government could negotiate an enabling arrangement with Russia but leave it to the private sector to execute. The Chennai-Vladivostok maritime connectivity corridor enhances scope for such cooperation.

This strategy would be a genuine win-win. India would contribute to its food security by reducing load on its resources (land, water, electricity) and providing opportunities to its excess farm labour. For Russia, dependency on China would come down, giving Moscow the strategic leverage that it needs and wants.

And here is where India needs to answer a strategic question. Is it willing to invest in the Russia story just as we celebrate Russia’s engagement with “Make in India”? India must write itself into the development text of the Far East and other parts of Russia through investments and expertise. There could be no stronger foundation for the relationship.

There is also an urgent need to overcome some recent angularities. The first is Afghanistan. At least till 15 August 2021, India and Russia had a serious disagreement, with Moscow unabashedly flirting with the Taliban. While both countries want stability in Afghanistan and curbs on export of terrorism and drugs, the perception in New Delhi is Moscow’s negotiators with the Taliban ended up become negotiators for the Taliban. That is a credibility problem for Russia to ponder.

India must write itself into the development text of the Far East and other parts of Russia through investments and expertise.

The second divergence is on the Indo-Pacific. It boils down to lack of trust. Russia does not trust India vis-à-vis the US, and India hears Russia reading from China’s script. This is a challenge to be addressed. Either country is the other’s flexibility mechanism, an arrangement that has stood the test of time. Russia’s ‘Greater Eurasia’ project and the Indo-Pacific are complementary and describe the same emergence: Of a new political moment and of a political geography that will seek a new alignment of interests and actors. Even as India and Russia carve new relationships, their sturdy partnership is a bank guarantee for both.

President Vladimir Putin’s visit to India is only his second trip abroad since the beginning of the pandemic. The first was to Geneva earlier this summer, for a summit with President Joe Biden. Coming to New Delhi to meet Prime Minister Narendra Modi is hugely symbolic and strategic. It indicates that the President knows India allows him a more equal partnership with China, even as Russia offers India room for its own endeavours.

In the Indo-Pacific and beyond, China’s growth in capabilities and political authoritarianism are now threatening to alter how we engage with technology and digital domains. China believes it has the right to access other nations’ information and networks without offering up access to its own. This is not a simple techno-mercantilism. There is a single purpose to China’s deepening investments in existing and future technologies: furthering the agenda of the Chinese Communist Party (CCP).

For Beijing, technology is about both national security and ideology. Under Xi Jinping, it will use the information age to rewrite every assumption of the postwar period. Countries outside China must join together to seek open, safe and inclusive technology and digital platforms and products.

There are five main ways in which we can shape national, regional and global engagement with our digital world. These must also drive the purpose and direction of the Quad countries (the United States, Australia, Japan and India) as they strive to create a technology and digital partnership in the Indo-Pacific.

‘China tech’ was for the CCP initially about managing the social contract within China. Now, the CCP is weaponising and gaming other nations’ democracies, public spheres and open systems. It is creating a digital insurgency that allows it to delegitimise its opponents on their own political turf. This goes beyond episodic interference in elections. The CCP uses American forums such as Twitter and Facebook to critique the domestic and foreign policy of nations such as India. Wolf warriors seek to shape the information space internationally while China and the CCP remain protected behind the Great Firewall. The unimpeded global access China is allowed under some perverse notion of free speech must be questioned; internet propaganda endorsed by authoritarian regimes cannot and should not go unchecked. As a first step, the world will have to embrace a political approach to repel the digital encroachments we are witnessing. The European Union offers a model – just as its General Data Protection Regulation sought to rein in the US technology giants, we need laws that limit China’s access to the public spheres of open societies, thereby curtailing its global influence.

Today, all digital (silk) roads lead to Beijing. Many developing countries rely on China for their technology sectors. From control over rare earths and key minerals to monopoly over manufacturing, China commands the digital spigot. The Quad countries and others in the Indo-Pacific must seek and encourage diversification. Affordable, accessible products and innovations must emerge in the digital space. From resilient supply chains to diversity of ownership, a whole new approach is needed to prevent the perverse influence of any single actor. This is the second way to shape global patterns of digital engagement.

The Chinese under Xi have embraced the dangerous essence of the Chinese phrase ‘borrowing a boat to go out to the sea’. The CPC has essentially borrowed all our boats to further their agenda.

Universities in the developed world, their media, their public institutions and even their technology companies are serving and responding to missives from the Middle Kingdom. Many journalists have exposed the Western media’s promiscuous entanglements with a Beijing that artfully co-opts them into its propaganda effort. In the digital age, this cannot be ignored. Countries will soon be faced with a digital fait accompli – signing on to Pax Sinica. As a third way to enhance engagement, it is time to protect liberal institutions from their own excesses.

China has attempted to internationalise its currency with the launch of its own digital currency. After banning financial institutions and payment companies from providing crypto-related services in May, China launched a crackdown on computer-powered crypto mining in June, and a blanket ban on all crypto transactions and mining in September, clearing the way for its digital renminbi (digital RMB). With the development of its own central bank digital currency, the Chinese government will now have the power to track spending in real time. It will have access to the entire digital footprint of a citizen or a company. This will provide Beijing with an unprecedented vault of data, which it can use to exercise control over technology companies and individuals.

The rise of China’s digital RMB has the potential to challenge the status of the American greenback. For decades, the US dollar has been the world’s dominant reserve currency. Yet countries such as Iran, Russia and Venezuela have already begun using the Chinese yuan for trade-related activities or replacing the dollar with the yuan as reference currency. China can shape all three attributes of the ‘ideal’ currency, also referred to as the ‘Impossible Trinity’: free capital flow, a fixed exchange rate and independent monetary policy. It is a matter of time before it uses currency as part of its wider geopolitical plans. And with its past experiments with many countries on ‘trade in local currency’, it will have the capacity to create disruptions in the global monetary system. This can only be countered with two measures: one, depoliticising the existing dollar-led currency arrangements (the tendency to weaponise the SWIFT system – a giant messaging network used by banks and other financial institutions to transmit secure information – and to employ ad-hoc economic sanctions) and two, investing in the economic future of the emerging economies that currently depend on China.

Lastly, China is seeking technological domination not only terrestrially but also in outer space. China has invested considerably in space technology and engages in counterspace activities. These include suspected interference in satellite operations, both through cyberattacks and ground-based lasers. There are growing fears that Chinese technologies developed for ostensibly peaceful uses, such as remote satellite repair and cleaning up debris, could be employed for nefarious ends. The inadequate space governance mechanisms is an opportunity for the Quad to develop situational awareness in the space realm to track and counter such activities, and to develop a new set of norms for space governance.

The Quad’s agenda is prescribed by China’s actions. It will have to be a political actor and have the capacity to challenge China in the information sphere and the technology domain. It will need to be a normative power and develop ideas and ideals that are attractive to all.

From codes and norms for financial technologies to the code of conduct for nations and corporations in cyberspace and outer space, the Quad has the responsibility and opportunity to write the rules for our common digital future.

The Quad will also have to be an economic actor and build strategic capacities and assets in the region and beyond. It will have to secure minerals, diversify supply chains and create alternatives that ensure the digital lifelines are not disrupted.

Most importantly, the Quad will need to be an attractive partner for others to work with. This is its best means to counter China’s dangerous influence.

Progress, as the world has designed and defined it, requires material production which, in turn, requires energy. Historically, therefore, fossil fuels like coal were key in economic growth across geographies. Today, the developed economies stand on the edifice of fossil fuels, carbon-intensive industries, and lifestyles that have resulted in global warming. The same growth path is now being questioned, and the poor and developing countries are being asked to build, find, and fund newer low- and no-carbon models to lift their people out of poverty and achieve their development goals.

As global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

Consequently, there are growing calls for India to declare a net-zero year: To offset its carbon emissions by various processes of GHG absorption and removal. India is aware that such calls are irrational, and despite international pressure, has avoided making pledges or setting hard targets, beyond its commitments at the Paris Climate Conference in 2015. Indeed, “net zero” is not possible with India’s current levels of reliance on coal. Its shift away from this fuel will depend largely on the quantum of additional money and resources that can be invested into alternative energy. However, as global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

In August 2020, UN Secretary-General António Guterres urged India to give up coal immediately. He asked that the country refrain from making any new thermal power investments after 2020, and criticised its decision to hold auctions for 41 coal blocks earlier that year. Similarly, in March this year, in a message to the Powering Past Coal Alliance Summit, the Secretary-General urged all governments to “end the deadly addiction to coal” by cancelling all global coal projects in the pipeline. Pre-pandemic, India had the second largest pipeline of new coal projects in the world. He also called the phasing out of coal from the electricity sector “the single most important step to get in line with the 1.5-degree goal of the Paris Agreement.”

For much of human history, photosynthesis was the primary source of mechanical energy. Human and animal muscles powered by food and fodder, made the world go around. Photosynthesis was also at the root of heat energy derived from burning wood. Eventually, coal replaced wood as the dominant source of heat energy, but still represented the energy of photosynthesis stockpiled over hundreds of years. The advent of the steam engine in the 17th century helped humans change the heat energy released from coal, to mechanical energy.

This development also upended the paradigm of material production. According to a recent estimate, coal was accounting for well over 90 percent of energy consumption in England by the mid-19th century, owing in large part to the steam engine. For long, researchers had been divided over the question of whether coal was pivotal to the industrial revolution. Scholars such as Wrigley (2010) regarded the switch to coal as a “necessary condition for the industrial revolution,” while others like Mokyr (2009) held that the “Industrial Revolution did not absolutely ‘need’ steam…nor was steam power absolutely dependent on coal.”

A November 2020 paper by Fernihough and O’Rourke might just settle the question: Using a database of European cities spanning the centuries from 1300 to 1900, the authors found that those located closer to coal fields were more likely to grow faster. Those cities, the researchers wrote, “located 49 km from the nearest coalfield grew 21.1 percent faster after 1750 than cities located 85 km further away.”

This article explores this line of enquiry by examining the consumption of coal across developed and developing countries, and mapping it against key metrics of energy transition. It finds that countries such as India—with their high dependence on coal and a simultaneous growth spurt in renewables—can be the most effective location for climate finance. This is plausible given that per capita coal consumption in India is still far below that of the developed world, and economic transitions are both inevitable and required to be ‘green’.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-COVID-19 recovery; the same is true for China. Consequently, there is growing scepticism in developed countries, that both India and China will double down on coal and increase production to overcome supply challenges in the future. While such concerns are not unwarranted, they are not unique to the developing world.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-COVID-19 recovery; the same is true for China.

Germany, for instance, in the first six months of 2021 ramped up its coal-based generation, which contributed 27 percent of the country’s electricity demand. Three factors contributed to this rise: Increase in energy demand amidst the successive waves of the COVID-19 pandemic, increased prices of natural gas, and reduction in electricity generation from renewable energy (particularly wind). Coal is often the bedrock of energy generation, and its use is impacted by complex market processes that cannot be reduced to normative choices.

Energy Use and Coal

Countries of the Organisation for Economic Cooperation and Development (OECD) are using progressively less energy to power their societies. Multiple factors can contribute to this trend, at least in theory. First is the technical improvements in energy efficiency—i.e., the use of less energy to perform the same tasks. Second is the “activity effect”, or the changes in energy use because of changes in economic activity. This would also encompass a “structure effect” which relates to changes in the mix of human activities that are prompted by changes in sectoral activity, such as transportation. And finally, there could be weather-related changes in energy use—for instance, more temperate weather can reduce the need for heating or cooling.

The IEA quantifies these effects, and consistently finds that the reduction in energy consumption in the OECD countries is largely a result of technical improvements in energy efficiency. This means that the reduced use of energy in advanced countries is not on account of any significant changes in consumer behaviour—otherwise, the activity effect would be the primary determinant of the fall in energy use. While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals. Consequently, the Agency has advocated for “urgent action” to counteract the slowing rate of improvement observed since 2015.

While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals.

Conversely, developing countries have seen a rapid rise in energy use owing to the activity effect (see Table 1). The increase in economic activity in the developing world is also directly correlated to improvements in life spans and socio-economic progress. While energy use has approximately doubled in countries like India and China from 2005, a large share of global energy efficiency savings is also driven by technical improvements in these countries. However, in the aftermath of the 2008-09 global financial crisis, China implemented a stimulus package that “shifted its manufacturing sector to more energy intensive manufacturing.” A similar trend may emerge in China’s recovery from the pandemic, that may reduce efficiency gains in the future.

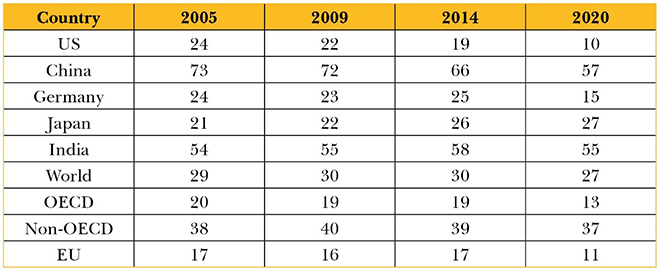

It would appear that OECD countries have managed to cut their dependence on coal over the last 15 years quite precipitously. In particular, this seems true of countries like the US and EU members. Japan, meanwhile, is an outlier, having turned to coal to provide base-load power to substitute nuclear energy. In most years between 2005 and 2020, the fall in coal consumption in OECD countries has outpaced the decline in total energy consumption. In 2020, for instance, coal consumption dropped by around 18 percent whereas total energy consumption fell by around 8 percent.

While China has begun to reduce its dependence on coal, it still accounts for the largest share of coal consumption amongst all nations. China is also home to over half of the world’s thermal power plant pipelines—with around 163 GW in pre-construction stage, even discounting the 484GW worth of cancellations since the Conference of Parties at Paris in 2015. China is also one of the last of the biggest providers of public finance for overseas power plants with over 40GW of projects in the pre-construction pipeline.

Simultaneously, coal consumption has remained relatively stable at just under 40 percent of primary energy consumption amongst non-OECD nations (see Table 2). In these countries, coal consumption tends to mirror total energy consumption. For instance, in 2018 and 2019, total energy consumption increased by three and two percentage points, respectively. India’s dependence on coal has also remained unvarying. These trends suggest that non-OECD countries such as India require to do much more to contribute to a global reduction in coal consumption and therefore towards net-zero GHG emissions. However, there is more to the OECD’s reduced coal consumption than meets the eye.

Table 2: Share of Coal in Primary Energy Consumption (%)

Country

2005

2009

2014

2020

US

24

22

19

10

China

73

72

66

57

Germany

24

23

25

15

Japan

21

22

26

27

India

54

55

58

55

World

29

30

30

27

OECD

20

19

19

13

Non-OECD

38

40

39

37

EU

17

16

17

11

Source: BP Statistical Review of World Energy, 2021 and author’s own calculations

Since the Earth Summit in 1992, India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions. This approach has often been subject to cross-examination by OECD experts. For instance, in a 2019 report by the Universal Ecological Fund, high-profile experts including a former White House Adviser and a Harvard professor, ranked national climate commitments based on absolute emission curtailment targets. The report clubbed developed and developing countries together in its assessment of the general insufficiency of climate pledges to meet the Paris Agreement’s goal to keep global warming below 1.5 degrees Celsius above pre-industrialisation levels.[1] This should not be a surprise, however, as it is only in consonance with the overall trend of Western academic discourse seeking to dilute the equity principle.

India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions.

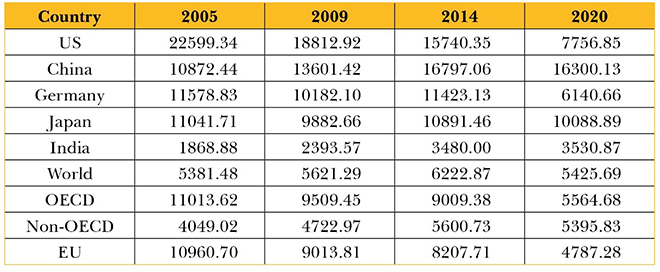

It is a principle that should not be set aside just yet, given the persistent differences in per capita fossil fuel consumption between the developed and developing worlds. Despite near doubling over 2005–2020, India’s per capita coal consumption is still below the global average (see Table 3). The global average, in turn, has remained static around this period because the decrease in the per capita consumption of coal in OECD countries has been partially offset by an increase in the per capita consumption in non-OECD countries. However, the per capita consumption of coal in OECD countries still exceeds that of non-OECD countries, despite much higher levels of wealth and, therefore, capability to transition to renewables and other fuels.

Table 3: Total per capita Coal Consumption (KWh)

Country

2005

2009

2014

2020

US

22599.34

18812.92

15740.35

7756.85

China

10872.44

13601.42

16797.06

16300.13

Germany

11578.83

10182.10

11423.13

6140.66

Japan

11041.71

9882.66

10891.46

10088.89

India

1868.88

2393.57

3480.00

3530.87

World

5381.48

5621.29

6222.87

5425.69

OECD

11013.62

9509.45

9009.38

5564.68

Non-OECD

4049.02

4722.97

5600.73

5395.83

EU

10960.70

9013.81

8207.71

4787.28

Source: BP Statistical Review of World Energy, 2021; World Bank and authors’ own calculations

Indeed, a large share of the decrease in per capita coal consumption in OECD countries is driven by transition to fuels such as natural gas, that are used to generate electricity, particularly in countries like the US. It accounts for around a 34-percent share of primary energy consumption in the US, and 25 percent in the EU, compared to seven percent in India (and a similar share in China). In contrast, the share of gas in India’s energy mix is amongst the lowest in the world. Even as Prime Minister Narendra Modi wants to more than double the contribution of natural gas to 15 percent of India’s energy mix by 2030, the Petroleum Secretary has said that the country cannot rely on natural gas. There are several reasons, including high landed costs relative to coal, complex domestic pricing mechanisms, a lack of pipeline infrastructure and stable supply/ import linkages, and the inability of financially stressed electricity distributors to enter into “take or pay” contracts.

India, therefore, requires relatively greater and more aggressive investments in alternative sources of energy than its developed country counterparts that have had decades to transition to fuels like natural gas. Such financial flows to India can prove to be much more effective vehicles for a net-zero trajectory, compared to similar investments in other parts of the world with higher per capita exposure to coal and relatively slower transition pathways to renewables.

Around 72 percent of India’s GHG emissions are linked to its energy sector. It is clear, that if OECD countries are aiming to accelerate a global reduction in GHG emissions, they will need to help India finance its energy transition and overcome the many resource-linked barriers to the wide-scale adoption of renewables. The high costs associated with renewable energy storage and grid upgrade requirements, are related resource challenges. Since developed countries are unlikely to be satisfied with per capita equity, they would do well to help India hurdle some of its obstacles.

Financing Energy Transition

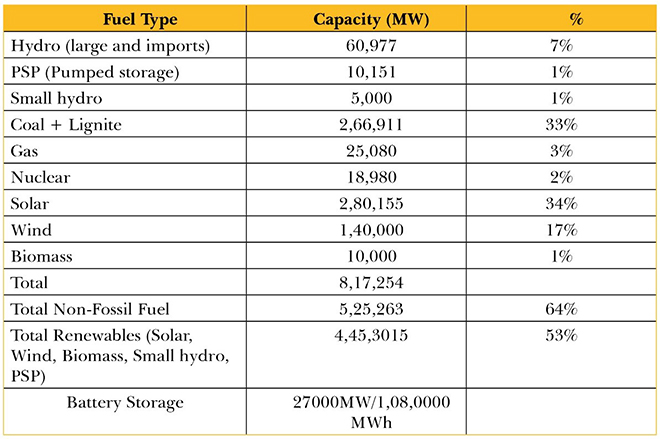

According to India’s Central Electricity Authority’s (CEA) Optimal Generation Capacity Mix, the country’s installed capacity will increase to 817 GW with an additional 27GW of battery storage, by 2029–30 (see Table 4). Of this, firm capacity will contribute approximately 395 GW while renewable sources, around 445 GW. Additionally, a July 2021 study has concluded that more efficient use of existing thermal resources could lead to 50 GW of excess coal capacity with respect to current needs of the system. With limited expectations from nuclear and gas resources and deteriorating coal economics, investments in renewable energy storage options are crucial for managing India’s base load requirements. This requires unlocking of financial and technological flows from the OECD, particularly since there are several uncertainties associated with the cost of battery storage technology. These include risks linked to supply chains and exchange rates.

Total Renewables (Solar, Wind, Biomass, Small hydro, PSP)

4,45,3015

53%

Battery Storage

27000MW/1,08,0000 MWh

Source: Central Electricity Authority; The cost trajectory for battery energy storage system is assumed to be reducing uniformly from 7 Cr in 2021-22 to 4.3 Cr (with basic battery cost of US $75/kWh) in 2029-30 for a four-hour battery system

The technologies that will pave the way to such low-coal path are developing rapidly, with significant progress in renewables, battery storage, and green hydrogen, amongst others. They each require, however, large financial outlays. Moreover, India is still highly dependent on expensive bank lending, which is now hitting sectoral exposure limits, whereas long-term capital is required to finance energy infrastructure. As of April 2020, the exposure of banks and non-bank financial institutions to India’s power sector was already around US$ 160 billion, roughly the lending necessary to finance the country’s renewable energy targets for 2030.

According to the Government of India’s ‘Energy Compact’ submitted to the UN in September 2021, the country required a total investment of US $221 billion to set up 450 GW renewable generation capacity, including associated transmission and storage systems. However, other research has pegged this investment much higher at US $661 billion, to build both renewable energy systems and transmission and distribution systems. The IEA also estimates that India requires a total investment of US $1.4 trillion for clean technologies to help achieve a sustainable development path till 2040. In comparison, developed countries managed a transition away from coal over a longer period of time and with different costs. Investments for clean energy in the Global South needs to be consistently and significantly higher to help achieve the simultaneous goals of SDG 7 (Affordable and Clean Energy) and other development targets.

Advanced countries would do well to recognise that long-term institutional capital is urgently required to help India transition from coal to renewables at scale. What is needed is far more than lip service; nor will change happen only through negotiations at Glasgow at the COP26. Overall, mainstream sources of international climate finance such as the Green Climate Fund and the Global Environment Facility have managed to provide just over a billion dollars in finance for national projects. While there is enthusiasm around green bond financing, the absolute value of issuances towards relevant segments such as renewable energy, is still relatively low at around US $11.2 billion since 2014. To put it in context, the global issuance of green bonds totalled over US $305 billion in 2020 alone, specifically for climate-related and sustainability projects.

India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

A high sensitivity to the cost of capital means that other sources of institutional capital are needed to fill the gap, even as the Indian private sector learns to raise green bonds and co-develops green taxonomies with relevant parties. Most OECD financing towards renewables in developing countries is conducted through debt instruments. According to the International Renewable Energy Agency, cumulative transactions and financial flows from the OECD countries towards renewables development in the rest of the world reached US $253 billion between 2009–2019, of which around US $228 billion was in the form of debt. India accounted for just under US $11 billion of the amount, which is less than 5 percent of the cumulative debt finance by OECD countries.

Table: Cumulative Transactions by OECD Countries into Renewables (2009-2019, %)

Debt

90

Grants

5

Equity and Shares in Collectives

4

Guarantees and Others

1

Source: International Renewable Energy Agency

OECD members must aim to redirect institutional investments towards India. For instance, their sovereign funds and pension funds must adjust to new business models around energy storage and distribution. There are also many possible designs of new financial instruments that could be explored. These could recognise the different capacities and capabilities in developing countries at the outset. For instance, grants and debt funding could be combined in multiple ways to subsidise loans. The scale of grant involvement could be directly proportionate to relevant environmental, social and governance factors, and therefore could incentivise more aggressive low-carbon paths. Similarly, new kinds of investment management and rating modalities could be employed to scale up investments where they are most required to offset planetary risks. The availability of innovative long-term finance for India is critical to any meaningful realisation of global net-zero ambitions. India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

Conclusion

India’s current per capita coal consumption is three-fifths that of the OECD average, and one-fifth that of China’s. This low per-capita coal consumption in a coal-rich country can and must remain the key feature of India’s growth, going forward. This article demonstrates, that for India to keep its coal in the ground, more and better financing is needed.

A market case for a green transition in India already exists. The last few years have demonstrated India’s appetite, amongst the public and the political class, for a move towards cleaner growth. What it requires now is what this essay calls for: A higher flow of capital towards crucial green sectors—in particular, a higher level of foreign capital inflows towards these sectors, and a better texture of such capital, moving towards a more patient and equitable finance.

Progress as the world has designed and defined it requires material production which, in turn, requires energy. Historically, therefore, fossil fuels like coal were key in economic growth across geographies. Today the developed economies stand on the edifice of fossil fuels, carbon-intensive industries and lifestyles that have resulted in global warming. The same growth path is now being questioned, and the poor and developing countries are being asked to build, find and fund newer low- and no-carbon models to lift their people out of poverty and achieve their development goals.

Consequently, there are growing calls for India to declare a net-zero year: to offset its carbon emissions by various processes of GHG absorption and removal. India is aware that such calls are irrational, and despite international pressure, has avoided making pledges or setting hard targets, beyond its commitments at the Paris climate conference in 2015. Indeed, “net zero” is not possible with India’s current levels of reliance on coal. Its shift away from this fuel will depend largely on the quantum of additional money and resources that can be invested into alternative energy. However, as global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

In August 2020, UN Secretary-General António Guterres urged India to give up coal immediately. He asked that the country refrain from making any new thermal power investments after 2020, and criticised its decision to hold auctions for 41 coal blocks earlier that year. Similarly, in March this year, in a message to the Powering Past Coal Alliance Summit, the Secretary-General urged all governments to “end the deadly addiction to coal” by cancelling all global coal projects in the pipeline.[1] Pre-pandemic, India had the second largest pipeline of new coal projects in the world. He also called the phasing out of coal from the electricity sector “the single most important step to get in line with the 1.5-degree goal of the Paris Agreement.”[2]

For much of human history, photosynthesis was the primary source of mechanical energy.[3] Human and animal muscles powered by food and fodder, made the world go around. Photosynthesis was also at the root of heat energy derived from burning wood. Eventually, coal replaced wood as the dominant source of heat energy, but still represented the energy of photosynthesis stockpiled over hundreds of years. The advent of the steam engine in the 17th century helped humans change the heat energy released from coal, to mechanical energy.

This development also upended the paradigm of material production. According to a recent estimate, coal was accounting for well over 90 percent of energy consumption in England by the mid-19th century, owing in large part to the steam engine.[4] For long, researchers had been divided over the question of whether coal was pivotal to the industrial revolution. Scholars such as Wrigley (2010) regarded the switch to coal as a “necessary condition for the industrial revolution,” while others like Mokyr (2009) held that the “Industrial Revolution did not absolutely ‘need’ steam…nor was steam power absolutely dependent on coal.”

A November 2020 paper by Fernihough and O’Rourke might just have settled the question: Using a database of European cities spanning the centuries from 1300 to 1900, the authors found that those located closer to coal fields were more likely to grow faster.[5] Those cities, the researchers wrote, “located 49 km from the nearest coalfield grew 21.1 percent faster after 1750 than cities located 85 km further away.”

It is no wonder then, that in March this year, International Energy Agency (IEA) chief Fatih Birol said it will not be fair to ask developing nations like India to stop using coal without giving international financial assistance to address the economic challenges that will result from such a move.[6] He noted that “many countries, so-called advanced economies, came to this industrialised levels and income levels by using a lot of coal,” and named the United States, Europe, and Japan.

This article explores this line of enquiry by examining the consumption of coal across developed and developing countries, and mapping it against key metrics of energy transition. It finds that countries such as India—with their high dependence on coal and a simultaneous growth spurt in renewables—can be the most effective location for climate finance. This is plausible given that per capita coal consumption in India is still far below that of the developed world, and economic transitions are both inevitable and required to be ‘green’.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-Covid-19 recovery; the same is true for China.[7] Consequently, there is growing scepticism in developed countries, that both India and China will double down on coal and increase production to overcome supply challenges in the future. While such concerns are not unwarranted, they are not unique to the developing world.

Germany, for instance, in the first six months of 2021 ramped up its coal-based generation, which contributed 27 percent of the country’s electricity demand.[8] Three factors contributed to this rise: increase in energy demand amidst the successive waves of the Covid-19 pandemic, increased prices of natural gas, and reduction in electricity generation from renewable energy (particularly wind.) Coal is often the bedrock of energy generation, and its use is impacted by complex market processes that cannot be reduced to normative choices.

Energy Use and Coal

Countries of the Organisation for Economic Cooperation and Development (OECD) are using progressively less energy to power their societies. Multiple factors can contribute to this trend, at least in theory. First is the technical improvements in energy efficiency – i.e., the use of less energy to perform the same tasks. Second is the “activity effect”, or the changes in energy use because of changes in economic activity. This would also encompass a “structure effect” which relates to changes in the mix of human activities that are prompted by changes in sectoral activity, such as transportation. And finally, there could be weather-related changes in energy use – for instance, more temperate weather can reduce the need for heating or cooling.

The IEA quantifies these effects, and consistently finds that the reduction in energy consumption in the OECD countries is largely a result of technical improvements in energy efficiency. This means that the reduced use of energy in advanced countries is not on account of any significant changes in consumer behaviour—otherwise, the activity effect would be the primary determinant of the fall in energy use. While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals. Consequently, the Agency has advocated for “urgent action” to counteract the slowing rate of improvement observed since 2015.[9]