In the Indo-Pacific and beyond, China’s growth in capabilities and political authoritarianism are now threatening to alter how we engage with technology and digital domains. China believes it has the right to access other nations’ information and networks without offering up access to its own. This is not a simple techno-mercantilism. There is a single purpose to China’s deepening investments in existing and future technologies: furthering the agenda of the Chinese Communist Party (CCP).

For Beijing, technology is about both national security and ideology. Under Xi Jinping, it will use the information age to rewrite every assumption of the postwar period. Countries outside China must join together to seek open, safe and inclusive technology and digital platforms and products.

There are five main ways in which we can shape national, regional and global engagement with our digital world. These must also drive the purpose and direction of the Quad countries (the United States, Australia, Japan and India) as they strive to create a technology and digital partnership in the Indo-Pacific.

‘China tech’ was for the CCP initially about managing the social contract within China. Now, the CCP is weaponising and gaming other nations’ democracies, public spheres and open systems. It is creating a digital insurgency that allows it to delegitimise its opponents on their own political turf. This goes beyond episodic interference in elections. The CCP uses American forums such as Twitter and Facebook to critique the domestic and foreign policy of nations such as India. Wolf warriors seek to shape the information space internationally while China and the CCP remain protected behind the Great Firewall. The unimpeded global access China is allowed under some perverse notion of free speech must be questioned; internet propaganda endorsed by authoritarian regimes cannot and should not go unchecked. As a first step, the world will have to embrace a political approach to repel the digital encroachments we are witnessing. The European Union offers a model – just as its General Data Protection Regulation sought to rein in the US technology giants, we need laws that limit China’s access to the public spheres of open societies, thereby curtailing its global influence.

Today, all digital (silk) roads lead to Beijing. Many developing countries rely on China for their technology sectors. From control over rare earths and key minerals to monopoly over manufacturing, China commands the digital spigot. The Quad countries and others in the Indo-Pacific must seek and encourage diversification. Affordable, accessible products and innovations must emerge in the digital space. From resilient supply chains to diversity of ownership, a whole new approach is needed to prevent the perverse influence of any single actor. This is the second way to shape global patterns of digital engagement.

The Chinese under Xi have embraced the dangerous essence of the Chinese phrase ‘borrowing a boat to go out to the sea’. The CPC has essentially borrowed all our boats to further their agenda.

Universities in the developed world, their media, their public institutions and even their technology companies are serving and responding to missives from the Middle Kingdom. Many journalists have exposed the Western media’s promiscuous entanglements with a Beijing that artfully co-opts them into its propaganda effort. In the digital age, this cannot be ignored. Countries will soon be faced with a digital fait accompli – signing on to Pax Sinica. As a third way to enhance engagement, it is time to protect liberal institutions from their own excesses.

China has attempted to internationalise its currency with the launch of its own digital currency. After banning financial institutions and payment companies from providing crypto-related services in May, China launched a crackdown on computer-powered crypto mining in June, and a blanket ban on all crypto transactions and mining in September, clearing the way for its digital renminbi (digital RMB). With the development of its own central bank digital currency, the Chinese government will now have the power to track spending in real time. It will have access to the entire digital footprint of a citizen or a company. This will provide Beijing with an unprecedented vault of data, which it can use to exercise control over technology companies and individuals.

The rise of China’s digital RMB has the potential to challenge the status of the American greenback. For decades, the US dollar has been the world’s dominant reserve currency. Yet countries such as Iran, Russia and Venezuela have already begun using the Chinese yuan for trade-related activities or replacing the dollar with the yuan as reference currency. China can shape all three attributes of the ‘ideal’ currency, also referred to as the ‘Impossible Trinity’: free capital flow, a fixed exchange rate and independent monetary policy. It is a matter of time before it uses currency as part of its wider geopolitical plans. And with its past experiments with many countries on ‘trade in local currency’, it will have the capacity to create disruptions in the global monetary system. This can only be countered with two measures: one, depoliticising the existing dollar-led currency arrangements (the tendency to weaponise the SWIFT system – a giant messaging network used by banks and other financial institutions to transmit secure information – and to employ ad-hoc economic sanctions) and two, investing in the economic future of the emerging economies that currently depend on China.

Lastly, China is seeking technological domination not only terrestrially but also in outer space. China has invested considerably in space technology and engages in counterspace activities. These include suspected interference in satellite operations, both through cyberattacks and ground-based lasers. There are growing fears that Chinese technologies developed for ostensibly peaceful uses, such as remote satellite repair and cleaning up debris, could be employed for nefarious ends. The inadequate space governance mechanisms is an opportunity for the Quad to develop situational awareness in the space realm to track and counter such activities, and to develop a new set of norms for space governance.

The Quad’s agenda is prescribed by China’s actions. It will have to be a political actor and have the capacity to challenge China in the information sphere and the technology domain. It will need to be a normative power and develop ideas and ideals that are attractive to all.

From codes and norms for financial technologies to the code of conduct for nations and corporations in cyberspace and outer space, the Quad has the responsibility and opportunity to write the rules for our common digital future.

The Quad will also have to be an economic actor and build strategic capacities and assets in the region and beyond. It will have to secure minerals, diversify supply chains and create alternatives that ensure the digital lifelines are not disrupted.

Most importantly, the Quad will need to be an attractive partner for others to work with. This is its best means to counter China’s dangerous influence.

Progress, as the world has designed and defined it, requires material production which, in turn, requires energy. Historically, therefore, fossil fuels like coal were key in economic growth across geographies. Today, the developed economies stand on the edifice of fossil fuels, carbon-intensive industries, and lifestyles that have resulted in global warming. The same growth path is now being questioned, and the poor and developing countries are being asked to build, find, and fund newer low- and no-carbon models to lift their people out of poverty and achieve their development goals.

As global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

Consequently, there are growing calls for India to declare a net-zero year: To offset its carbon emissions by various processes of GHG absorption and removal. India is aware that such calls are irrational, and despite international pressure, has avoided making pledges or setting hard targets, beyond its commitments at the Paris Climate Conference in 2015. Indeed, “net zero” is not possible with India’s current levels of reliance on coal. Its shift away from this fuel will depend largely on the quantum of additional money and resources that can be invested into alternative energy. However, as global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

In August 2020, UN Secretary-General António Guterres urged India to give up coal immediately. He asked that the country refrain from making any new thermal power investments after 2020, and criticised its decision to hold auctions for 41 coal blocks earlier that year. Similarly, in March this year, in a message to the Powering Past Coal Alliance Summit, the Secretary-General urged all governments to “end the deadly addiction to coal” by cancelling all global coal projects in the pipeline. Pre-pandemic, India had the second largest pipeline of new coal projects in the world. He also called the phasing out of coal from the electricity sector “the single most important step to get in line with the 1.5-degree goal of the Paris Agreement.”

For much of human history, photosynthesis was the primary source of mechanical energy. Human and animal muscles powered by food and fodder, made the world go around. Photosynthesis was also at the root of heat energy derived from burning wood. Eventually, coal replaced wood as the dominant source of heat energy, but still represented the energy of photosynthesis stockpiled over hundreds of years. The advent of the steam engine in the 17th century helped humans change the heat energy released from coal, to mechanical energy.

This development also upended the paradigm of material production. According to a recent estimate, coal was accounting for well over 90 percent of energy consumption in England by the mid-19th century, owing in large part to the steam engine. For long, researchers had been divided over the question of whether coal was pivotal to the industrial revolution. Scholars such as Wrigley (2010) regarded the switch to coal as a “necessary condition for the industrial revolution,” while others like Mokyr (2009) held that the “Industrial Revolution did not absolutely ‘need’ steam…nor was steam power absolutely dependent on coal.”

A November 2020 paper by Fernihough and O’Rourke might just settle the question: Using a database of European cities spanning the centuries from 1300 to 1900, the authors found that those located closer to coal fields were more likely to grow faster. Those cities, the researchers wrote, “located 49 km from the nearest coalfield grew 21.1 percent faster after 1750 than cities located 85 km further away.”

This article explores this line of enquiry by examining the consumption of coal across developed and developing countries, and mapping it against key metrics of energy transition. It finds that countries such as India—with their high dependence on coal and a simultaneous growth spurt in renewables—can be the most effective location for climate finance. This is plausible given that per capita coal consumption in India is still far below that of the developed world, and economic transitions are both inevitable and required to be ‘green’.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-COVID-19 recovery; the same is true for China. Consequently, there is growing scepticism in developed countries, that both India and China will double down on coal and increase production to overcome supply challenges in the future. While such concerns are not unwarranted, they are not unique to the developing world.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-COVID-19 recovery; the same is true for China.

Germany, for instance, in the first six months of 2021 ramped up its coal-based generation, which contributed 27 percent of the country’s electricity demand. Three factors contributed to this rise: Increase in energy demand amidst the successive waves of the COVID-19 pandemic, increased prices of natural gas, and reduction in electricity generation from renewable energy (particularly wind). Coal is often the bedrock of energy generation, and its use is impacted by complex market processes that cannot be reduced to normative choices.

Energy Use and Coal

Countries of the Organisation for Economic Cooperation and Development (OECD) are using progressively less energy to power their societies. Multiple factors can contribute to this trend, at least in theory. First is the technical improvements in energy efficiency—i.e., the use of less energy to perform the same tasks. Second is the “activity effect”, or the changes in energy use because of changes in economic activity. This would also encompass a “structure effect” which relates to changes in the mix of human activities that are prompted by changes in sectoral activity, such as transportation. And finally, there could be weather-related changes in energy use—for instance, more temperate weather can reduce the need for heating or cooling.

The IEA quantifies these effects, and consistently finds that the reduction in energy consumption in the OECD countries is largely a result of technical improvements in energy efficiency. This means that the reduced use of energy in advanced countries is not on account of any significant changes in consumer behaviour—otherwise, the activity effect would be the primary determinant of the fall in energy use. While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals. Consequently, the Agency has advocated for “urgent action” to counteract the slowing rate of improvement observed since 2015.

While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals.

Conversely, developing countries have seen a rapid rise in energy use owing to the activity effect (see Table 1). The increase in economic activity in the developing world is also directly correlated to improvements in life spans and socio-economic progress. While energy use has approximately doubled in countries like India and China from 2005, a large share of global energy efficiency savings is also driven by technical improvements in these countries. However, in the aftermath of the 2008-09 global financial crisis, China implemented a stimulus package that “shifted its manufacturing sector to more energy intensive manufacturing.” A similar trend may emerge in China’s recovery from the pandemic, that may reduce efficiency gains in the future.

It would appear that OECD countries have managed to cut their dependence on coal over the last 15 years quite precipitously. In particular, this seems true of countries like the US and EU members. Japan, meanwhile, is an outlier, having turned to coal to provide base-load power to substitute nuclear energy. In most years between 2005 and 2020, the fall in coal consumption in OECD countries has outpaced the decline in total energy consumption. In 2020, for instance, coal consumption dropped by around 18 percent whereas total energy consumption fell by around 8 percent.

While China has begun to reduce its dependence on coal, it still accounts for the largest share of coal consumption amongst all nations. China is also home to over half of the world’s thermal power plant pipelines—with around 163 GW in pre-construction stage, even discounting the 484GW worth of cancellations since the Conference of Parties at Paris in 2015. China is also one of the last of the biggest providers of public finance for overseas power plants with over 40GW of projects in the pre-construction pipeline.

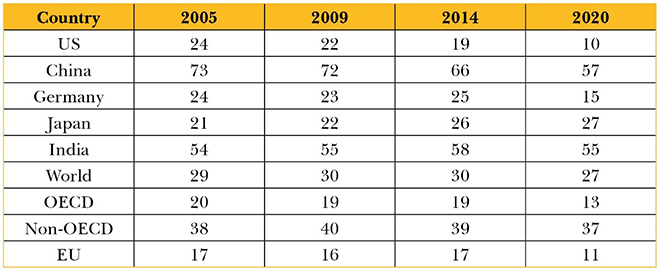

Simultaneously, coal consumption has remained relatively stable at just under 40 percent of primary energy consumption amongst non-OECD nations (see Table 2). In these countries, coal consumption tends to mirror total energy consumption. For instance, in 2018 and 2019, total energy consumption increased by three and two percentage points, respectively. India’s dependence on coal has also remained unvarying. These trends suggest that non-OECD countries such as India require to do much more to contribute to a global reduction in coal consumption and therefore towards net-zero GHG emissions. However, there is more to the OECD’s reduced coal consumption than meets the eye.

Table 2: Share of Coal in Primary Energy Consumption (%)

Country

2005

2009

2014

2020

US

24

22

19

10

China

73

72

66

57

Germany

24

23

25

15

Japan

21

22

26

27

India

54

55

58

55

World

29

30

30

27

OECD

20

19

19

13

Non-OECD

38

40

39

37

EU

17

16

17

11

Source: BP Statistical Review of World Energy, 2021 and author’s own calculations

Since the Earth Summit in 1992, India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions. This approach has often been subject to cross-examination by OECD experts. For instance, in a 2019 report by the Universal Ecological Fund, high-profile experts including a former White House Adviser and a Harvard professor, ranked national climate commitments based on absolute emission curtailment targets. The report clubbed developed and developing countries together in its assessment of the general insufficiency of climate pledges to meet the Paris Agreement’s goal to keep global warming below 1.5 degrees Celsius above pre-industrialisation levels.[1] This should not be a surprise, however, as it is only in consonance with the overall trend of Western academic discourse seeking to dilute the equity principle.

India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions.

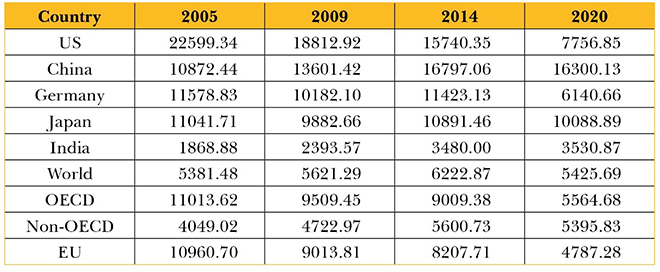

It is a principle that should not be set aside just yet, given the persistent differences in per capita fossil fuel consumption between the developed and developing worlds. Despite near doubling over 2005–2020, India’s per capita coal consumption is still below the global average (see Table 3). The global average, in turn, has remained static around this period because the decrease in the per capita consumption of coal in OECD countries has been partially offset by an increase in the per capita consumption in non-OECD countries. However, the per capita consumption of coal in OECD countries still exceeds that of non-OECD countries, despite much higher levels of wealth and, therefore, capability to transition to renewables and other fuels.

Table 3: Total per capita Coal Consumption (KWh)

Country

2005

2009

2014

2020

US

22599.34

18812.92

15740.35

7756.85

China

10872.44

13601.42

16797.06

16300.13

Germany

11578.83

10182.10

11423.13

6140.66

Japan

11041.71

9882.66

10891.46

10088.89

India

1868.88

2393.57

3480.00

3530.87

World

5381.48

5621.29

6222.87

5425.69

OECD

11013.62

9509.45

9009.38

5564.68

Non-OECD

4049.02

4722.97

5600.73

5395.83

EU

10960.70

9013.81

8207.71

4787.28

Source: BP Statistical Review of World Energy, 2021; World Bank and authors’ own calculations

Indeed, a large share of the decrease in per capita coal consumption in OECD countries is driven by transition to fuels such as natural gas, that are used to generate electricity, particularly in countries like the US. It accounts for around a 34-percent share of primary energy consumption in the US, and 25 percent in the EU, compared to seven percent in India (and a similar share in China). In contrast, the share of gas in India’s energy mix is amongst the lowest in the world. Even as Prime Minister Narendra Modi wants to more than double the contribution of natural gas to 15 percent of India’s energy mix by 2030, the Petroleum Secretary has said that the country cannot rely on natural gas. There are several reasons, including high landed costs relative to coal, complex domestic pricing mechanisms, a lack of pipeline infrastructure and stable supply/ import linkages, and the inability of financially stressed electricity distributors to enter into “take or pay” contracts.

India, therefore, requires relatively greater and more aggressive investments in alternative sources of energy than its developed country counterparts that have had decades to transition to fuels like natural gas. Such financial flows to India can prove to be much more effective vehicles for a net-zero trajectory, compared to similar investments in other parts of the world with higher per capita exposure to coal and relatively slower transition pathways to renewables.

Around 72 percent of India’s GHG emissions are linked to its energy sector. It is clear, that if OECD countries are aiming to accelerate a global reduction in GHG emissions, they will need to help India finance its energy transition and overcome the many resource-linked barriers to the wide-scale adoption of renewables. The high costs associated with renewable energy storage and grid upgrade requirements, are related resource challenges. Since developed countries are unlikely to be satisfied with per capita equity, they would do well to help India hurdle some of its obstacles.

Financing Energy Transition

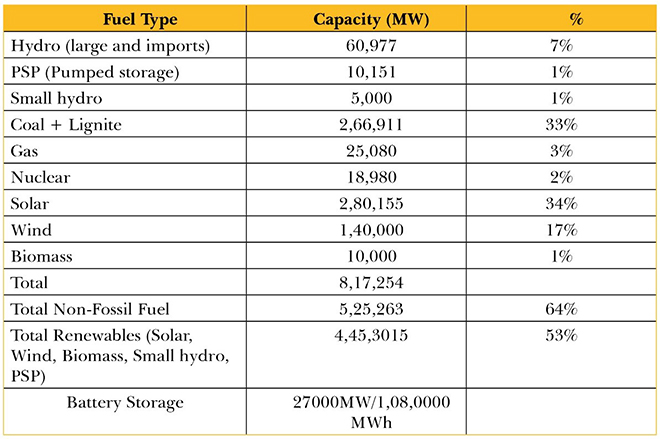

According to India’s Central Electricity Authority’s (CEA) Optimal Generation Capacity Mix, the country’s installed capacity will increase to 817 GW with an additional 27GW of battery storage, by 2029–30 (see Table 4). Of this, firm capacity will contribute approximately 395 GW while renewable sources, around 445 GW. Additionally, a July 2021 study has concluded that more efficient use of existing thermal resources could lead to 50 GW of excess coal capacity with respect to current needs of the system. With limited expectations from nuclear and gas resources and deteriorating coal economics, investments in renewable energy storage options are crucial for managing India’s base load requirements. This requires unlocking of financial and technological flows from the OECD, particularly since there are several uncertainties associated with the cost of battery storage technology. These include risks linked to supply chains and exchange rates.

Total Renewables (Solar, Wind, Biomass, Small hydro, PSP)

4,45,3015

53%

Battery Storage

27000MW/1,08,0000 MWh

Source: Central Electricity Authority; The cost trajectory for battery energy storage system is assumed to be reducing uniformly from 7 Cr in 2021-22 to 4.3 Cr (with basic battery cost of US $75/kWh) in 2029-30 for a four-hour battery system

The technologies that will pave the way to such low-coal path are developing rapidly, with significant progress in renewables, battery storage, and green hydrogen, amongst others. They each require, however, large financial outlays. Moreover, India is still highly dependent on expensive bank lending, which is now hitting sectoral exposure limits, whereas long-term capital is required to finance energy infrastructure. As of April 2020, the exposure of banks and non-bank financial institutions to India’s power sector was already around US$ 160 billion, roughly the lending necessary to finance the country’s renewable energy targets for 2030.

According to the Government of India’s ‘Energy Compact’ submitted to the UN in September 2021, the country required a total investment of US $221 billion to set up 450 GW renewable generation capacity, including associated transmission and storage systems. However, other research has pegged this investment much higher at US $661 billion, to build both renewable energy systems and transmission and distribution systems. The IEA also estimates that India requires a total investment of US $1.4 trillion for clean technologies to help achieve a sustainable development path till 2040. In comparison, developed countries managed a transition away from coal over a longer period of time and with different costs. Investments for clean energy in the Global South needs to be consistently and significantly higher to help achieve the simultaneous goals of SDG 7 (Affordable and Clean Energy) and other development targets.

Advanced countries would do well to recognise that long-term institutional capital is urgently required to help India transition from coal to renewables at scale. What is needed is far more than lip service; nor will change happen only through negotiations at Glasgow at the COP26. Overall, mainstream sources of international climate finance such as the Green Climate Fund and the Global Environment Facility have managed to provide just over a billion dollars in finance for national projects. While there is enthusiasm around green bond financing, the absolute value of issuances towards relevant segments such as renewable energy, is still relatively low at around US $11.2 billion since 2014. To put it in context, the global issuance of green bonds totalled over US $305 billion in 2020 alone, specifically for climate-related and sustainability projects.

India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

A high sensitivity to the cost of capital means that other sources of institutional capital are needed to fill the gap, even as the Indian private sector learns to raise green bonds and co-develops green taxonomies with relevant parties. Most OECD financing towards renewables in developing countries is conducted through debt instruments. According to the International Renewable Energy Agency, cumulative transactions and financial flows from the OECD countries towards renewables development in the rest of the world reached US $253 billion between 2009–2019, of which around US $228 billion was in the form of debt. India accounted for just under US $11 billion of the amount, which is less than 5 percent of the cumulative debt finance by OECD countries.

Table: Cumulative Transactions by OECD Countries into Renewables (2009-2019, %)

Debt

90

Grants

5

Equity and Shares in Collectives

4

Guarantees and Others

1

Source: International Renewable Energy Agency

OECD members must aim to redirect institutional investments towards India. For instance, their sovereign funds and pension funds must adjust to new business models around energy storage and distribution. There are also many possible designs of new financial instruments that could be explored. These could recognise the different capacities and capabilities in developing countries at the outset. For instance, grants and debt funding could be combined in multiple ways to subsidise loans. The scale of grant involvement could be directly proportionate to relevant environmental, social and governance factors, and therefore could incentivise more aggressive low-carbon paths. Similarly, new kinds of investment management and rating modalities could be employed to scale up investments where they are most required to offset planetary risks. The availability of innovative long-term finance for India is critical to any meaningful realisation of global net-zero ambitions. India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

Conclusion

India’s current per capita coal consumption is three-fifths that of the OECD average, and one-fifth that of China’s. This low per-capita coal consumption in a coal-rich country can and must remain the key feature of India’s growth, going forward. This article demonstrates, that for India to keep its coal in the ground, more and better financing is needed.

A market case for a green transition in India already exists. The last few years have demonstrated India’s appetite, amongst the public and the political class, for a move towards cleaner growth. What it requires now is what this essay calls for: A higher flow of capital towards crucial green sectors—in particular, a higher level of foreign capital inflows towards these sectors, and a better texture of such capital, moving towards a more patient and equitable finance.

It is no secret that Washington is bullish about the idea of fostering closer ties with India in an effort to counter China. But tighter ties takes two. Is Washington, DC’s enthusiasm matched in New Delhi?

“We know that we don’t share a typical Atlantic-style relationship. It’s a more Asian relationship, more grays than black and whites in our relationship,” Samir Saran, the president of the Observer Research Foundation, an Indian think tank in New Delhi, told me.

Dating back to the Cold War, India has maintained a formal policy of non-alignment. In reality, though, the Soviet Union, which supported India in the 1971 Indo-Pakistani War and provided the vast majority of its defence equipment, earned India’s support and sympathy. The US, meanwhile, was seen as an untrustworthy and unreliable actor; nor did it help that America was close to India’s neighbour and foe, Pakistan.

In recent years, however, relations between India and the US have improved. There are many reasons for this, but the most important one is arguably a rising China, which America is seeking to counter and contain by working with other countries, and with India in particular. Pakistan, meanwhile, cooperates closely with China.

A year after the US president Joe Biden’s election, and with China at the top of America’s foreign policy agenda, I turned to Saran to ask how, exactly, policymakers in New Delhi perceive US overtures, particularly given the fact that, historically, America has been seen as a less than reliable partner.

“I think much of what you sometimes may hear in Delhi or in DC could possibly be remnants of the 20th century, people holding on to positions of the past, people who have written books on India’s behaviour or American attitudes to the past, wanting to still be relevant in the 21st century,” he said. “I think there is a more pragmatic assessment of each other today.”

Still, he added, “I’m not saying that we trust the Americans all the time.”

One area in which America and India have traditionally not seen eye to eye is in India’s immediate neighbourhood, including Afghanistan. “I think the Americans had to leave [Afghanistan],” Saran told me. “Could they have left better? I think all of us would agree, yes. It was a bit of a messy withdrawal. I don’t think any amount of spin can change that.” He also noted that India could have been consulted, though added that Delhi has always seen America maintain a certain distance from India on Afghanistan. “And in that sense, it’s not surprising. It’s not that we’ve been let down heartbroken because America did not consult us.” In other words, the events of this summer were not enough to deter India from cooperating with the US.

Relatedly, if China is bringing India and the US together, some have wondered if Russia might tear them apart.

“Russia punches above its weight in terms of global affairs,” said Saran. “Russia is going to remain a relevant voice. And we do not want a situation where we paint Putin into the Chinese corner. I think that would be disastrous for us. So we will have to find ways in which we can accommodate Russia.

“I think that is now visible to all in DC, we have not let that come in the way of being more bold, more ambitious, more forward-looking with our American partners.”

This is, broadly speaking, true, though there are some in Washington who feel differently: for example, John Bolton, former president Donald Trump’s national security adviser, penned an op-ed in the Hill on 10 November in which he argued that India’s purchase of S-400 air defence systems from Russia “raises serious obstacles to closer politico-military relations between Washington and New Delhi”. Saran, unsurprisingly, sees it differently, painting a picture in which India can help the US by developing economic ties with Russia, thus moving Moscow away from Beijing.

Even issues as weighty as US-China or India-Russia relations, however, seem small next to the existential issue of our age: climate change. India is already battling air pollution and will be profoundly impacted by the climate crisis. Is there a sense there that America is not doing enough?

India, he told me, has been a strong proponent of climate justice, equity, and action. And this is an area where the US and India can “work together and create a new framework that would catalyse trillions of dollars of green capital to flow into green projects”. He didn’t mean aid or grants, he stressed. “We are talking about commercial capital from banks… We are talking about creating a whole new green financial ecosystem.”

And what about the gap between India’s rhetoric and, say, the reality of air pollution in Delhi? How does that gap close?

“The gap closes like it was closed in New York and London, by more advanced, cleaner, greener systems,” he said. “We are going to have to go through that decade of pain.”

The painful period would hurt less if it was accelerated, he acknowledged. Still, some element of what India will go through to get to the other, better, greener side will require discomfort. The same could perhaps be said of the US-India relationship itself.

Progress as the world has designed and defined it requires material production which, in turn, requires energy. Historically, therefore, fossil fuels like coal were key in economic growth across geographies. Today the developed economies stand on the edifice of fossil fuels, carbon-intensive industries and lifestyles that have resulted in global warming. The same growth path is now being questioned, and the poor and developing countries are being asked to build, find and fund newer low- and no-carbon models to lift their people out of poverty and achieve their development goals.

Consequently, there are growing calls for India to declare a net-zero year: to offset its carbon emissions by various processes of GHG absorption and removal. India is aware that such calls are irrational, and despite international pressure, has avoided making pledges or setting hard targets, beyond its commitments at the Paris climate conference in 2015. Indeed, “net zero” is not possible with India’s current levels of reliance on coal. Its shift away from this fuel will depend largely on the quantum of additional money and resources that can be invested into alternative energy. However, as global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

In August 2020, UN Secretary-General António Guterres urged India to give up coal immediately. He asked that the country refrain from making any new thermal power investments after 2020, and criticised its decision to hold auctions for 41 coal blocks earlier that year. Similarly, in March this year, in a message to the Powering Past Coal Alliance Summit, the Secretary-General urged all governments to “end the deadly addiction to coal” by cancelling all global coal projects in the pipeline.[1] Pre-pandemic, India had the second largest pipeline of new coal projects in the world. He also called the phasing out of coal from the electricity sector “the single most important step to get in line with the 1.5-degree goal of the Paris Agreement.”[2]

For much of human history, photosynthesis was the primary source of mechanical energy.[3] Human and animal muscles powered by food and fodder, made the world go around. Photosynthesis was also at the root of heat energy derived from burning wood. Eventually, coal replaced wood as the dominant source of heat energy, but still represented the energy of photosynthesis stockpiled over hundreds of years. The advent of the steam engine in the 17th century helped humans change the heat energy released from coal, to mechanical energy.

This development also upended the paradigm of material production. According to a recent estimate, coal was accounting for well over 90 percent of energy consumption in England by the mid-19th century, owing in large part to the steam engine.[4] For long, researchers had been divided over the question of whether coal was pivotal to the industrial revolution. Scholars such as Wrigley (2010) regarded the switch to coal as a “necessary condition for the industrial revolution,” while others like Mokyr (2009) held that the “Industrial Revolution did not absolutely ‘need’ steam…nor was steam power absolutely dependent on coal.”

A November 2020 paper by Fernihough and O’Rourke might just have settled the question: Using a database of European cities spanning the centuries from 1300 to 1900, the authors found that those located closer to coal fields were more likely to grow faster.[5] Those cities, the researchers wrote, “located 49 km from the nearest coalfield grew 21.1 percent faster after 1750 than cities located 85 km further away.”

It is no wonder then, that in March this year, International Energy Agency (IEA) chief Fatih Birol said it will not be fair to ask developing nations like India to stop using coal without giving international financial assistance to address the economic challenges that will result from such a move.[6] He noted that “many countries, so-called advanced economies, came to this industrialised levels and income levels by using a lot of coal,” and named the United States, Europe, and Japan.

This article explores this line of enquiry by examining the consumption of coal across developed and developing countries, and mapping it against key metrics of energy transition. It finds that countries such as India—with their high dependence on coal and a simultaneous growth spurt in renewables—can be the most effective location for climate finance. This is plausible given that per capita coal consumption in India is still far below that of the developed world, and economic transitions are both inevitable and required to be ‘green’.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-Covid-19 recovery; the same is true for China.[7] Consequently, there is growing scepticism in developed countries, that both India and China will double down on coal and increase production to overcome supply challenges in the future. While such concerns are not unwarranted, they are not unique to the developing world.

Germany, for instance, in the first six months of 2021 ramped up its coal-based generation, which contributed 27 percent of the country’s electricity demand.[8] Three factors contributed to this rise: increase in energy demand amidst the successive waves of the Covid-19 pandemic, increased prices of natural gas, and reduction in electricity generation from renewable energy (particularly wind.) Coal is often the bedrock of energy generation, and its use is impacted by complex market processes that cannot be reduced to normative choices.

Energy Use and Coal

Countries of the Organisation for Economic Cooperation and Development (OECD) are using progressively less energy to power their societies. Multiple factors can contribute to this trend, at least in theory. First is the technical improvements in energy efficiency – i.e., the use of less energy to perform the same tasks. Second is the “activity effect”, or the changes in energy use because of changes in economic activity. This would also encompass a “structure effect” which relates to changes in the mix of human activities that are prompted by changes in sectoral activity, such as transportation. And finally, there could be weather-related changes in energy use – for instance, more temperate weather can reduce the need for heating or cooling.

The IEA quantifies these effects, and consistently finds that the reduction in energy consumption in the OECD countries is largely a result of technical improvements in energy efficiency. This means that the reduced use of energy in advanced countries is not on account of any significant changes in consumer behaviour—otherwise, the activity effect would be the primary determinant of the fall in energy use. While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals. Consequently, the Agency has advocated for “urgent action” to counteract the slowing rate of improvement observed since 2015.[9]

Conversely, developing countries have seen a rapid rise in energy use owing to the activity effect (see Table 1). The increase in economic activity in the developing world is also directly correlated to improvements in life spans and socio-economic progress. While energy use has approximately doubled in countries like India and China from 2005, a large share of global energy efficiency savings is also driven by technical improvements in these countries. However, in the aftermath of the 2008-09 global financial crisis, China implemented a stimulus package that “shifted its manufacturing sector to more energy intensive manufacturing.”[10] A similar trend may emerge in China’s recovery from the pandemic, that may reduce efficiency gains in the future.

Table 1: Total Energy Consumption (Exajoules)

Source: BP Statistical Review of World Energy, 2021[11]

Equity in Coal

It would appear that OECD countries have managed to cut their dependence on coal over the last 15 years quite precipitously. In particular, this seems true of countries like the US and EU members. Japan, meanwhile, is an outlier, having turned to coal to provide base-load power to substitute nuclear energy. In most years between 2005 and 2020, the fall in coal consumption in OECD countries has outpaced the decline in total energy consumption. In 2020, for instance, coal consumption dropped by around 18 percent whereas total energy consumption fell by around eight percent.

While China has begun to reduce its dependence on coal, it still accounts for the largest share of coal consumption among all nations. China is also home to over half of the world’s thermal power plant pipelines – with around 163 GW in pre-construction stage, even discounting the 484GW worth of cancellations since the Conference of Parties at Paris in 2015.[12] China is also one of the last of the biggest providers of public finance for overseas power plants with over 40GW of projects in the pre-construction pipeline.

Simultaneously, coal consumption has remained relatively stable at just under 40 percent of primary energy consumption among non-OECD nations (see Table 2). In these countries, coal consumption tends to mirror total energy consumption. India’s dependence on coal has also remained unvarying. These trends suggest that non-OECD countries such as India require to do much more to contribute to a global reduction in coal consumption and therefore towards net-zero GHG emissions. However, there is more to the OECD’s reduced coal consumption than meets the eye.

Table 2: Share of Coal in Primary Energy Consumption (%)

Source: BP Statistical Review of World Energy, 2021 and authors’ own calculations

Since the Earth Summit in 1992, India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions. This approach has often been subject to cross-examination by OECD experts. For instance, in a 2019 report by the Universal Ecological Fund, high-profile experts including a former White House Adviser and a Harvard professor, ranked national climate commitments based on absolute emission curtailment targets.[13] The report clubbed developed and developing countries together in its assessment of the general insufficiency of climate pledges to meet the Paris Agreement’s goal to keep global warming below 1.5 degrees Celsius above pre-industrialisation levels.[14] This should not be a surprise, however, as it is only in consonance with the overall trend of Western academic discourse seeking to dilute the equity principle.

It is a principle that should not be set aside just yet, given the persistent differences in per capita fossil fuel consumption between the developed and developing worlds. Despite near doubling over 2005-2020, India’s per capita coal consumption is still below the global average (see Table 3). The global average, in turn, has remained static around this period because the decrease in the per capita consumption of coal in OECD countries has been partially offset by an increase in the per capita consumption in non-OECD countries. However, the per capita consumption of coal in OECD countries still exceeds that of non-OECD countries, despite much higher levels of wealth and, therefore, greater capability to transition to renewables and other fuels.

Table 3: Total per capita Coal Consumption (KWh)

Source: BP Statistical Review of World Energy, 2021; World Bank and authors’ own calculations

Indeed, a large share of the decrease in per capita coal consumption in OECD countries is driven by transition to fuels such as natural gas, that are used to generate electricity, particularly in countries like the US. It accounts for around a 34-percent share of primary energy consumption in the US, and 25 percent in the EU, compared to seven percent in India (and a similar share in China). In contrast, the share of gas in India’s energy mix is among the lowest in the world. Even as Prime Minister Narendra Modi wants to more than double the contribution of natural gas to 15 percent of India’s energy mix by 2030, the Petroleum Secretary has said that the country cannot rely on natural gas.[15] There are several reasons, including high landed costs relative to coal, complex domestic pricing mechanisms, a lack of pipeline infrastructure and stable supply/ import linkages, and the inability of financially stressed electricity distributors to enter into “take or pay” contracts.[16]

India, therefore, requires relatively greater and more aggressive investments in alternative sources of energy than its developed country counterparts that have had decades to transition to fuels like natural gas. Such financial flows to India can prove to be much more effective vehicles for a net-zero trajectory, compared to similar investments in other parts of the world with higher per capita exposure to coal and relatively slower transition pathways to renewables.

Around 72 percent of India’s GHG emissions are linked to its energy sector.[17] It is clear, that if OECD countries are aiming to accelerate a global reduction in GHG emissions, they will need to help India finance its energy transition and overcome the many resource-linked barriers to the wide-scale adoption of renewables. The high costs associated with renewable energy storage and grid upgrade requirements, are related resource challenges. Since developed countries are unlikely to be satisfied with per capita equity, they would do well to help India hurdle some of its obstacles.

Financing Energy Transition

According to India’s Central Electricity Authority’s (CEA) Optimal Generation Capacity Mix, the country’s installed capacity will increase to 817 GW with an additional 27GW of battery storage, by 2029-30 (see Table 4). Of this, firm capacity will contribute approximately 395 GW while renewable sources, around 445 GW. Additionally, a July 2021 study has concluded that more efficient use of existing thermal resources could lead to 50 GW of excess coal capacity with respect to current needs of the system.[18] With limited expectations from nuclear and gas resources and deteriorating coal economics, investments in renewable energy storage options are crucial for managing India’s base load requirements. This requires unlocking of financial and technological flows from the OECD, particularly since there are several uncertainties associated with the cost of battery storage technology. These include risks linked to supply chains and exchange rates.

Source: Central Electricity Authority; The cost trajectory for battery energy storage system is assumed to be reducing uniformly from 7 Cr in 2021-22 to 4.3 Cr (with basic battery cost of $75/kWh) in 2029-30 for a 4-hour battery system

Experts point out that the more renewable energy is introduced into the grid, “the harder and more expensive it will be to use” because of inherent factors such as intermittency.[19] This will need to be offset by investments in a grid that is able to accommodate variable and increased flows of electricity across different regions. The IEA estimates that annual investments in electricity grids will need to “more than double” by 2030 in a conservative scenario where developed countries achieve net zero by 2050, China around 2060, and other emerging and developing economies, by 2070, at the latest.[20] India will also need to explore much wider scale of privatisation of state distribution companies, which now owe generators around USD 20 billion.[21]

The capacity utilisation of India’s coal assets has also witnessed a significant decline over the past decade, with power plants running at 53.37 percent plant load factor (PLF) in FY 2020-21 compared to 77.5 percent in FY 2009-10.[22] Several factors have contributed to this, including the rapidly expanding share of renewable energy generation. India’s coal story is beset with additional challenges including planned decommissioning of older coal plants (approximately 54 GW of coal plants by 2030).[23] Research indicates that the cost of retirement ranges between[24] USD 0.41 – 0.59 million per MW, with older thermal units relatively cheaper to decommission. Consequently, maintaining India’s coal fleet also requires around USD 106 million in investments, to retrofit existing thermal power plants with Flue Gas Desulphurization units. The deadline for doing so has been extended several times in the past decade and has finally been fixed for 2022 for plants located in populous areas.[25] The combination of underutilised coal plants, increasing costs of plant maintenance and reduction in costs of renewables, provides a unique opportunity to galvanise investments and strategic attention towards a low-coal pathway.

The technologies that will pave the way to such low-coal path are developing rapidly, with significant progress in renewables, battery storage, and green hydrogen, among others. They each require, however, large financial outlays. Moreover, India is still highly dependent on expensive bank lending, which is now hitting sectoral exposure limits, whereas long-term capital is required to finance energy infrastructure. As of April 2020, the exposure of banks and non-bank financial institutions to India’s power sector was already around USD 160 billion, roughly the lending necessary to finance the country’s renewable energy targets for 2030. [26]

According to the Government of India’s ‘Energy Compact’ submitted to the UN in September 2021, the country required a total investment of USD 221 billion to set up 450 GW renewable generation capacity, including associated transmission and storage systems.[27] However, other research has pegged this investment much higher at USD 661 billion, to build both renewable energy systems and transmission and distribution systems.[28] The IEA also estimates that India requires a total investment of USD 1.4 trillion for clean technologies to help achieve a sustainable development path till 2040.[29] In comparison, developed countries managed a transition away from coal over a longer period of time and with different costs. Investments for clean energy in the Global South need to be consistently and significantly higher to help achieve the simultaneous goals of SDG 7 (Affordable and Clean Energy) and other development targets.

Advanced countries would do well to recognise that long-term institutional capital is urgently required to help India transition from coal to renewables at scale. What is needed is far more than lip service; nor will change happen only through negotiations at Glasgow at the COP26. Overall, mainstream sources of international climate finance such as the Green Climate Fund and the Global Environment Facility have managed to provide just over a billion dollars in finance for national projects.[30] While there is enthusiasm around green bond financing, the absolute value of issuances towards relevant segments such as renewable energy, is still relatively low at around USD 11.2 billion since 2014.[31] To put it in context, the global issuance of green bonds totalled over USD 305 billion in 2020 alone, specifically for climate-related and sustainability projects.[32]

A high sensitivity to the cost of capital means that other sources of institutional capital are needed to fill the gap, even as the Indian private sector learns to raise green bonds and co-develops green taxonomies with relevant parties. Most OECD financing towards renewables in developing countries is conducted through debt instruments. According to the International Renewable Energy Agency, cumulative transactions and financial flows from the OECD countries towards renewables development in the rest of the world reached USD 253 billion between 2009-2019, of which around USD 228 billion was in the form of debt. India accounted for just under USD 11 billion of the amount, which is less than five percent of the cumulative debt finance by OECD countries.

Table 5: Cumulative Transactions by OECD Countries into Renewables (2009-2019, %)

Source: International Renewable Energy Agency

OECD members must aim to redirect institutional investments towards India. For instance, their sovereign funds and pension funds must adjust to new business models around energy storage and distribution. There are also many possible designs of new financial instruments that could be explored. These could recognise the different capacities and capabilities in developing countries at the outset. For instance, grants and debt funding could be combined in multiple ways to subsidise loans. The scale of grant involvement could be directly proportionate to relevant environmental, social and governance factors, and therefore could incentivise more aggressive low-carbon paths. Similarly, new kinds of investment management and rating modalities could be employed to scale up investments where they are most required to offset planetary risks. The availability of innovative long-term finance for India is critical to any meaningful realisation of global net-zero ambitions. India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

Conclusion

India’s current per capita coal consumption is three-fifths that of the OECD average, and one-fifth that of China’s. This low per-capita coal consumption in a coal-rich country can and must remain the key feature of India’s growth, going forward. This article demonstrates, that for India to keep its coal in the ground, more and better financing is needed.

A market case for a green transition in India already exists. The last few years have demonstrated India’s appetite, among the public and the political class, for a move towards cleaner growth. What it requires now is what this essay calls for: a higher flow of capital towards crucial green sectors—in particular, a higher level of foreign capital inflows towards these sectors, and a better texture of such capital, moving towards a more patient and equitable finance.

This brief was first published in ORF’s monograph, Shaping Our Green Future: Pathways and Policies for a Net-Zero Transformation, November 2021.