The emergence of new technologies has digitalised markets, societies and nations. Once perceived as a strength, this proliferation of technology is now also a vulnerability. It has made tech-governance more political and social, and less about the traditional modes of regulation such as permissions, standards and tariffs.

India is among the most technology adept nations, a function of its people’s comfort with IT products and services as well as its late-mover advantage. It must now engage with a spectrum of evolving needs around law and regulation. This is necessary to accelerate population-scale opportunities and address widespread risks.

Three sets of issues emerge here – understanding the nature of technology-linked risks; assessing the challenges to governance; and being imaginative in embracing new modes of regulation.

Three sets of issues emerge here – understanding the nature of technology-linked risks, assessing the challenges to governance, and being imaginative in embracing new modes of regulation.

Improved access is credited with enabling financial inclusion, efficiency in education and healthcare, and fostering local e-commerce as well as global trade. However, a large user base is also a double-edged sword. As a result, corrective interventions need to be nimble and at digital velocity and population scale. Legacy regulation is simply ineffective.

This is best illustrated by problems plaguing social media platforms. A 2021 study found a high rate of social media misinformation in India, and attributed this in part to the country’s higher Internet penetration rate, driven by smart phones. Between June-July 2021 alone, Facebook received 1,504 user complaints in India – with a significant proportion of these related to bullying, harassment or sexually inappropriate content. Concerns are also emerging across other digital ecosystems, such as online gambling and crypto-assets. The mobile phone is a communication device, a crime scene and also an unsafe personal space.

Several state-level laws regulate or entirely prohibit betting and gambling. However, research suggests India is among the top five countries in terms of income potential from online gambling, and that the domestic online casino market may grow by 22 per cent each year. People from several states, such as Maharashtra, Telangana and Karnataka, are among the most frequent visitors to online gambling websites. The market for illegal betting and gambling in India is highly lucrative, with some estimating its value at USD 150 billion.

Offshore gambling websites often channel black money, engage in illicit transactions and launder wealth through financial intermediaries. Their operators are invariably based outside India, which makes it difficult to enforce the writ of the state. Recent investigations by bodies like the Enforcement Directorate have revealed instances of locals being hired to open bank accounts and trade through various online wallets, revealing gaps in due diligence mechanisms.

For the digital economy to flourish, it is important to evolve approaches that help resolve systemic and structural risks. It is time to reassess what is good, what is bad and what is ugly in this new digital landscape. Online gaming and online gambling must not be conflated. Similarly blockchain and sensible DeFi must not be clubbed with predatory crypto-gaming. After all, if we don’t embrace disruptive technology markets through sensible regulation, others will. A failure to capitalise may see India lose key avenues for economic growth and investment. India risk environment will then be shaped by external jurisdictions, some inimical to the country.

For instance, there are approximately 15 million crypto-asset investors in India, with total holdings of INR 400 billion. However, the regulatory and policy uncertainty has compelled crypto-asset entrepreneurs and exchanges to look to operate in more favourable markets. Exchanges such as Cryptokart, Koinex and ZebPay have exited the Indian market. ZebPay, for instance, is now headquartered in Singapore. In late 2021, many crypto-asset founders in India were considering moving their businesses to either the UAE or Singapore.

What we need today is new thinking and a new imagination of the digital world as not merely a virtual extension of the real, but an entirely different paradigm.

By banning cryptocurrencies altogether, nations such as China have missed the bus. India must leverage its position as the world’s third-fastest growing technology hub and seize the opportunity created by Beijing’s command and control ethos that is antithetical to innovation. India can and should become a global norms shaper in tech.

Tech regulation at population scale is akin to writing a new constitution for a digital nation. What we need today is new thinking and a new imagination of the digital world as not merely a virtual extension of the real, but an entirely different paradigm. There needs to be a clear-eyed understanding of what is legal, what is illegal and what may be illegal and yet requires regulations to serve and protect users and citizens.

To use a real-world analogy, since the 1990s, many countries including India have consistently distributed condoms and undertook safety campaigns among sex-workers without legalising prostitution or made available safe syringes to drug users without legalising the act. For governments and regulators, the role is no longer one of a gatekeeper that has the ability to prevent or permit activities online; it is becoming more of an ecosystem shaper and reducer of public bads.

By taxing cryptocurrency assets but not recognising these as legal tender, India has shown some welcome flexibility. It would do well to retain this nimbleness and become a co-curator of relatively safe tech platforms, services and products of the future that respond to Indian jurisdiction rather that off-shore the production of risks along with the rewards.

The talk of values is not new to German foreign policy-makers. But the Russian invasion on Ukraine seems to have finally led Germany to walk the walk. The last week has been both frenzied and path-breaking in German politics.

On 22 February, Germany’s Chancellor, Olaf Scholz—a Social Democrat from Hamburg—called for a halt to Nord Stream 2, in response to Russian President, Vladimir Putin’s, provocations in Eastern Ukraine. This was dramatic at several levels: Germany’s energy dependence on Russia had tended to make some politicians—including Scholz’s predecessor, Angela Merkel (a Christian Democrat)—wary of pulling the plug on the pipeline project. Scholz deserves even more credit for having made this break with Germany’s Russia policy in the context of party politics: The Social Democrats had come under critique in the past for being too soft on Russia (Russlandversteher).

Germany’s difficult past had led it to ban the export of weapons to conflict-zones; in keeping with this practice, the country had blocked Estonia from sending arms to Ukraine last month.

Since the outbreak of war in Ukraine on 24 February, Olaf Scholz has taken three further remarkable steps. First, after some hesitation, he has agreed to the inclusion of a ban on SWIFT transactions with Russia. This is a strong and costly signal to send to Russia as it will also have financial implications for Germany. Second, Germany’s difficult past had led it to ban the export of weapons to conflict-zones; in keeping with this practice, the country had blocked Estonia from sending arms to Ukraine last month. Olaf Scholz engineered an unprecedented shift. In a stirring speech at a special session of the German Parliament on 27 February, Scholz stated that Germany, by supporting Ukraine, will stand on the side of Europe, democracy, and the “the right side of history”. Amongst the concrete measures he outlined, sending military supplies to Ukraine was key: “Russian invasion marks a turning point. It is our duty to support Ukraine to the best of our ability in defending against Putin’s invading army”. Germany will now be supplying anti-tank weapons and Stinger missiles to Ukraine. And third, just as significant is Germany’s announcement to increase its NATO defence spending, thereby signaling the emergence of Germany as a security actor.

In a country where deliberative democracy is exalted (sometimes to a point where it amounts to being a strategy to doing nothing or muddling through), and the burden of history is high, the swift turn towards taking greater responsibility through action cannot be underestimated. Scholz’s leadership has been critical to this development, though he is undoubtedly helped by his coalition partners in the Green Party, who have come to power on a platform of principles and values. Germany’s proactive role is invigorating for us to observe, and is perhaps also serving as a catalyst for the European Union: Witness the unprecedented decision by the EU to purchase weapons for Ukraine.

One could still take issue with the timing of all this: It would have indeed been better to signal such resolve to Putin before his attack on Ukraine, thereby, deterring war in the first place. But at a time when Germany seems to be finally walking the walk of values, it is time to not look behind, but fare forward.

Germany’s proactive role is invigorating for us to observe, and is perhaps also serving as a catalyst for the European Union: Witness the unprecedented decision by the EU to purchase weapons for Ukraine.

It is clear that Scholz has understood the importance of hard power, in a way that his predecessors had not. As a dedicated European, he also knows that the Putin’s aggression towards Ukraine is a threat to European security as a whole. The question remains though, will he be able to extend his gaze to the global stage, and exercise much-needed leadership there? Putin is not the only authoritarian with grand designs in his neighbourhood; President Xi has been displaying similar adventurism towards Taiwan. The Ukraine crisis has brought these two players even closer, thus far. Will Scholz be the Chancellor to break out of the European platitudes of “partner, competitor, and rival” and finally call out China, just the way he has with Russia? As Mayor of Hamburg, Scholz was able to successfully attract Chinese investment to his city. As the Chancellor of Germany, he now has the onerous task of building a governance architecture that will secure the continent—and like-minded, democratic partners—from Chinese expansionism.

In the third decade of the twenty-first century, democracies face a new adversary — technology. Technology was once seen as a force for good, which could bridge the gap between the state and restless streets. Today, owned and controlled by large enterprises and extra-territorial governments, that very technology sometimes undermines the foundations of democracy, where it functions as a public sphere and a vibrant information exchange.

Much of the world has blearily woken up to big tech’s ambitions, expansion and unaccountable power to shape the human condition. A few companies, dotted on America’s West Coast (henceforth referred to as big tech), now possess the ability to harness the digital gold rush — along with the equally overwhelming influence on discourse in democratic societies. In parallel, a rising China, with its rapid successes in building a vibrant technology ecosystem, has unleashed plans to dominate innovation, high technology and the global perceptions ecosystem (henceforth referred to as red tech).

Technology from the West Coast of the United States and technology that seeks to serve the Chinese Communist Party (CCP) have both chosen to pursue their defined objectives with little thought for constitutional systems and laws in third countries. As such, much of the democratic world is at risk of being caught in the vice-like grip of big tech and red tech. It is, therefore, time for democratic societies to discover and examine means to secure an open and free global technological ecosystem that serves all shades of democracy.

Technology from the West Coast of the United States and technology that seeks to serve the Chinese Communist Party (CCP) have both chosen to pursue their defined objectives with little thought for constitutional systems and laws in third countries.

Why the Battle for Tech Matters

The threat that big tech poses to democracy is multifaceted. First, major social media platforms — Twitter, Facebook, Google and others — curate, promote and curtail information received by and, indeed, even the opinions of citizens in democratic societies. This power over speech and expression, and therefore over our politics and polity, is unrivalled in history (Baer and Chin 2021). While US steel, big oil and big tobacco were brought to heel by domestic regulations and national governments, the transnational reach of big tech has made it much harder to circumscribe (Lago 2021).

Operating outside rules and regulations prescribed by sovereign constitutions, social media platforms now exercise a worrying level of influence without accountability. Big tech has deplatformed controversial political figures such as Donald Trump (Byers 2021); censored content, a decision that internal ombudsmen disagree with (Eidelman and Ruane 2021); and has encouraged an engagement-based content ranking system that has allowed everything from disinformation about coronavirus disease 2019 (COVID-19) to hate speech to spread (Harris 2021). Platforms are free to decide whether they function as private hosting platforms or providers of a vital public utility; they cannot be both. Yet, they pick and choose between the two functions as it suits them.

National governments have not been asleep at the wheel. From New Delhi to Canberra, they have tabled regulations to rein in social media behemoths. In every instance, platform enterprises have chosen to obstruct, obfuscate and outmanoeuvre regulatory efforts (Clayton 2021). Left unregulated, our digital commons may become a noxious space that suffocates democracy, rather than being the promised breath of fresh air.

The future of democratic societies will also be decided by the contest with China in high technology. This competition runs deeper than China’s desire to build “national champions” that can outcompete the Googles and Apples of the world. To Beijing, China’s technology capabilities directly serve interests, ideologies and inclinations of the CCP (Tyagi 2021). Even as the Great Firewall of China allows the CCP monopoly control over ideas and over truth among its own citizens, China’s ever-increasing reach and economic expansion provides the party the ability to pervert and undermine the public sphere of other nations.

Platforms are free to decide whether they function as private hosting platforms or providers of a vital public utility; they cannot be both.

From harnessing artificial intelligence (AI) in the form of facial recognition technologies to vastly expand its citizen surveillance system (Davies 2021) to deploying those very capabilities against Uighur minorities in Xinjiang (Mozur 2019), the CCP will not shy away from deploying tech to reinforce strict authoritarian control at home. Overseas, “wolf warriors” (Martin 2021) insert themselves into every global debate of consequence and Chinese money power prevents Western media or social media from acting against such insidious and troubling participation that aggravates cleavages in other societies.

As China’s economic influence and technological capabilities have grown, it has sought to influence and manipulate global publics. China’s official media, governmental entities and diplomats have leveraged open platforms such as Twitter to peddle disinformation on the origins of COVID-19 (Associated Press 2021). China’s influence operations have also extended to election interference in Taiwan (Kurlantzick 2019), and they are increasingly inserting themselves in other countries as well. According to Freedom House, China has used its technological capabilities, in tandem with its economic and political power, to launch a massive influence operation that is gaming democracies from the inside out (Cook 2020).

Red tech is clearly an extension of the CCP’s global ambitions. For example, global standards bodies and multilateral organizations have been flooded with standards proposals by Chinese tech firms that would enshrine CCP values into the fundamental architecture of the internet (Gargeyas 2021). At the United Nations, Huawei and other Chinese state-owned enterprises have led advocacy for a “New IP” to replace the existing TCP/IP (Transmission Control Protocol/Internet Protocol) structure of the internet (Gross and Murgia 2020). Industry analysts have expressed concern that this new structure, with inbuilt controls that would allow for vastly increased governmental interference, is fundamentally at odds with the open internet of today.

According to Freedom House, China has used its technological capabilities, in tandem with its economic and political power, to launch a massive influence operation that is gaming democracies from the inside out (Cook 2020).

The ascendance of Chinese standards and tech also worries global actors for other reasons. While the United States and the European Union have enabled the creation of penetrated and argumentative democracies — wherein all countries and civil society organizations can advocate for the regulation of big tech or the promulgation of General Data Protection Regulation (GDPR) standards — China has no equivalent political structure. In fact, China’s intemperate wolf warrior diplomacy, which has precipitated clashes with Australia (Ryan 2020), Sweden (BBC News 2018) and France (Seibt 2021), among others, demonstrates that China has little tolerance for dissenting views or for reciprocal tolerance of criticism.

The Regulatory Void

Despite the high stakes and clear threat, regulation has failed to keep up. Major powers have not come to the fundamental realization that regulations must be both political and functional. Technology regulations driven by industry may have prized functionality, but both big tech’s subversion of regular constitutional processes and democratic debate as well as red tech’s brazen advancement of the CCP’s agenda demand regulation to recognize and return to its political roots.

Part of the reluctance to commit to a more political vision of regulation stems from overdependence on a China that dominates major global economies and the tech innovation ecosystem (Pletka and Scissors 2020). Given the massive size of the Chinese market, its capable and growing technology product and service lines, and Beijing’s willingness to use market access as leverage, many dither in enforcing regulations that exclude Chinese technology from specific sectors and functions. Others feel that government interference and politicization in regulatory matters could result in the fracturing of the global tech innovation ecosystem altogether (Schneider-Petsinger et al. 2019).

Technology regulations driven by industry may have prized functionality, but both big tech’s subversion of regular constitutional processes and democratic debate as well as red tech’s brazen advancement of the CCP’s agenda demand regulation to recognize and return to its political roots.

However, the return to more political regulation to oversee technology in the days ahead is inevitable. Simply, it is part of a well-established historical cycle. As Caetano Penna (2022) points out, every technological revolution has generated cycles of exuberance that leave contemporary social forces and political institutions in disarray. Only later does society mobilize to reshape institutions to suit a new era. Such regulation in service of societal goals has always been a key determinant in the evolution of industrialized societies. The spread of communication technologies in the boom from the 1980s to 2008 represented a cycle of exuberance. Today, however, technology possesses the power to fundamentally remake, disrupt and destabilize societies. AI-enabled machines threaten to put millions out of work and social media platforms, with a little Chinese help, have the potential to undermine democracies.

What Does a More Political Vision Look Like?

States, civil societies and general publics will have to take back control of the conversation over technology from tech companies. Part of this process will be nationally led and the rest multilateral. Domestic polities need to debate and hammer out a national consensus on some key issues, including on whether to enshrine privacy as a fundamental right. Assuming privacy is guaranteed, what level of privacy would suit their purposes? Who should own and have access to data? Who decides, and through what process, whether particular ideologies and groups should have access to the public commons?

In parts of the world where this debate is ongoing, robust data protection and privacy laws have been framed. While Canada now holds major tech platforms to the same transparency standards as traditional broadcasting groups (Solomun, Polataiko and Hayes 2021), Australia (Choudhury 2021) and India (Saran 2021) have adopted more stringent social media rules aimed at forcing big tech to comply with national-level regulations and directives on content. Nations would also have to debate the merits and benefits of the existing open internet model versus competing visions such as China’s New IP proposal. Each of these decisions would require clear choices by citizens who have, thus far, been excluded from conversations by governing elites and technology companies.

Domestic polities need to debate and hammer out a national consensus on some key issues, including on whether to enshrine privacy as a fundamental right.

At the multilateral level, bringing politics back into regulation will help safeguard data and democracies. An excellent example of political regulation is the European GDPR data architecture. Even firms outside the European Union that provide services to EU citizens find themselves subject to the European Union’s fundamentally political vision of privacy for its citizens (Nadeau 2020). The GDPR has also allowed for another political choice: flows of data will be free within the European Union but will be subject to protections upon leaving its borders.1 In effect, the European Union has erected a robust regime of protection that privileges countries that share a similar vision of privacy and data protection.

The European Union’s economic, political and normative leverage, popularized through the “Brussels effect,” has effectively forced other regimes to make way for it, with numerous countries enacting similar procedures. As such, the European experience in norms and standards setting is useful. Countries that share similar political visions of internet governance, disinformation and other aspects of technology policy can come together multilaterally to make the vision prevail globally. And disruptive players such as China, still new to the standards game, must make their peace with liberal democratic norms — or risk being left out in the cold.

Robert Fay suggests key digital powers come together to form a multilateral body, the Digital Stability Board (DSB), which would enact digital policy in much the same way that the Financial Stability Board helps design and monitor the implementation of key financial policies while assessing risks and vulnerabilities in the global financial system (Emanuele 2021). A DSB would lead discussion on regulating data value chains, countering misinformation and the development of cutting-edge technologies such as AI (ibid.). Given the transnational nature of the challenge posed by big tech’s dominance, a forum such as the DSB would be well suited to lay down the rules of the road on regulation and reining in major tech platforms.

Countries that share similar political visions of internet governance, disinformation and other aspects of technology policy can come together multilaterally to make the vision prevail globally.

While such a DSB would be useful to manage hostilities with powers such as China, another interesting proposal comes in the form of a group of 1o leading democracies, or D10. Proposed by British Prime Minister Boris Johnson (Fisher 2020), a D10 grouping would significantly source equipment for key technologies such as 5G from countries within the partnership. It could also develop a shared approach on key threats facing democracies, including countering disinformation, penalizing purveyors of influence operations such as China (or even Russia and other countries) and devising workable regulations for social media platforms that strike a balance between fighting fake news and preserving freedom of expression.

Ultimately, the introduction of the D10 to digital policy debates would signify a shared political vision, born out of democratic values, toward building the digital economy and regulating malcontents in the system. Good, old-fashioned democratic politics remains a primary driver even in the digital age. Wolves and wolf warriors hunt in packs; open societies need to respond with similar unity of purpose.

This piece builds on an intervention by Samir Saran at the Summit for Democracy on December 10, 2021.

If a weary international community—reeling from unanticipated challenges and unprecedented disruptions in the early 21st century—was looking forward to a stabilising start to the 2020s, its hopes were short-lived. COVID-19 continues to weave its way through borders and continents, felling victims and flummoxing governments. Two years down the line, it is increasingly clear that we have to learn to live with the virus, as it shows signs of transitioning to become endemic. A “new normal” where COVID-19 does not cripple communities, countries and whole continents is the future, even as vaccine inequity makes the possibility of more lethal variants imminent.

But even before COVID-19 forced us to radically rethink and redo the way we live our very lives, a certain tiredness had been evident. Generational and geographical shifts in the balance of power, rapid advances in technology-led innovations, and existential global risks like climate change have all strained the capacity of prevailing international norms and institutions. These have left them looking wilted, if not withered. Now, these norms and institutions have all but shattered from the strain of the pandemic. There is no percentage in stating the obvious, yet it must be reiterated: The international community needs new ideas, anchors and torchbearers to reinvigorate globalisation and strengthen global co-operation.

Towards this end, only asinine assessments of a future world order as the century turns 20 would ignore the crucial role of India in shaping this decade, and determining the trajectory of the decades to follow. Our endeavour with this series of essays is to capture the ideas and ethics driving contemporary Indian diplomacy; examine the methods and contours of India’s engagement with the world; and, offer a prognosis of India’s future as a leading power.

Under the rubric of ‘India@75: Aspirations, Ambitions, and Approaches’, ORF has curated 18 essays written by some of the world’s finest minds, representing former heads of state and government, members of parliament, heads of international institutions, leaders from business, and experts from academia and media. Between them, they have studied India’s evolving relationship with new geographies, its engagement with new domains of global governance, and the human imperative that must define India’s rise.

Few predict the path ahead will be easy for India, or that latent and legacy challenges confronting this nation can be ignored. Indeed, most assessments in this volume suggest disquiet and uncertainty. Amrita Narlikar begins her essay with a cautionary note on world affairs. “Multilateralism is facing a crisis of unprecedented proportions,” she writes, “It manifests itself in a fundamental questioning of the very value of multilateralism within countries and deadlocks in negotiations in multilateral organisations.” But this global crisis, she argues, also begets opportunities for India. C. Raja Mohan agrees and asserts that this period of churn offers India the opportunity to shed the temptation to act alone and actively build new coalitions and consensus with other powers. But this will depend, he argues, on how quickly India can restructure its traditional worldview.

As Harsh V Pant writes in this essay, this restructuring is already underway, as “India’s past diffidence in making certain foreign policy choices is rapidly giving way to greater readiness to acknowledge the need for a radical shift in thinking about internal capability enhancement by leveraging external partnerships.”

As the world’s centre of gravity shifts from the Atlantic system, India’s engagement with both emerging and old geographies acquires new salience. And this is where the new external partnerships are actively taking shape. Central among these is the dynamically evolving Indo-Pacific construct which, as Premesha Saha posits, will weave communities, markets and states from the East Pacific to East Africa into one strategic geography. How India adapts its “economic structure” to these realities and implements its “commitment to prevent hegemony in the oceans”, argues Kwame Owino, will determine its ability to lead these new regions.

But shaping new geographies will also require India to manage certain old relationships. The Indo-Pacific should not be seen in isolation—its markets and communities are also rapidly integrating with the Eurasian supercontinent. Steven Blockmans laments that the India-EU relationship has underperformed given its potential to anchor democratic and rules-based governance in greater Eurasia. Solomon Passy and Angel Apostolov boldly make the case for exploring the possibility of a dialogue between NATO and India, indicating just how drastically—and rapidly—the mental maps of the world are morphing.

There is a common thread that binds these analyses: A keen interest in India’s evolving relationship with the US and China. These three nations will, after all, rank among the largest three economies by the middle of this century. The turbulent Twenties will see the dynamics of this power triangle assume centre stage. The US sees India as a partner in its endeavour to neutralise an increasingly aggressive and expansionist China. Jane Holl Lute argues that India “has understood China’s principal strategic aim to replace the United States as the most consequential security power in Asia”. While India’s choices will undoubtedly implicate the balance of power between the US and China, India will most likely chart its own course in international affairs.

ORF Distinguished Fellow Rajeswari Pillai Rajagopalan highlights India’s behaviour in international negotiations on outer space as a primary example. In every significant process—from the UN GGE to the EU CoC—India has argued for greater multilateralism while actively discouraging behaviour that is “inherently destabilising”. I would add India’s engagement on cyber governance, particularly on emerging technologies, to this list. Although technological systems are rapidly unravelling, India has sought to frame rules for its digital economy that both serve its development interests and preserve interdependence. As Trisha Ray writes, “New Delhi must prepare to shape, rather than be shaped, by these shifting geopolitical winds.” Others remind us that much work still needs to be done. Renato Flores urges India to learn lessons from its RCEP withdrawal, shed traditional hesitations, and emerge as a leading advocate for multilateral trade.

India’s most significant contribution to the global commons will be providing sustainable livelihoods to its own people, and its battle against climate change. Indeed, Oommen Kurian & ShobaSuri begin their analysis with the proposition that success or failure in implementing the global SDG agenda is dependent almost wholly on India achieving its own targets. India already produces nearly half of all global vaccines and is a leading voice on IPR reform, as Khor Swee Kheng & K. Srinath Reddy note, making it essential for global health security. India will also be tasked with achieving livelihood goals for itself and the world in a carbon-constrained world, which is why Jayant Sinha argues that India can no longer rely on the ‘farm to industry’ model of development.

Instead, Nilanjan Ghosh asserts that India’s own goal of becoming a US$10 trillion economy, which is both equitable and inclusive, is only possible by following through on the SDG agenda. All of this, according to Adil Zainulbhai, will be powered by India’s already immense digital infrastructure, innovation capabilities and skilled workforce as it leverages the Fourth Industrial Revolution to its advantage. “India’s green transformation,” asserts Mihir Sharma, “will have to be led by the decisions of its people and by the energy of its private sector.”

It is these twin imperatives—achieving sustainable development and the climate change agenda— that make India a very different type of ‘rising power’. Its path to prominence will not be defined by military dominance or coercive economic capabilities. Instead, India’s rise will be characterised by its ability to provide solutions, technologies and finance to emerging communities in urgent need of new models of economic growth and social mobility. It is this ‘new economic diplomacy’, Navdeep Suri believes, that will define India’s foreign policy priorities in the decade ahead.

Underwriting India’s foreign policy will be its civilisational identity as a democratic, open and plural society. Arguably the most abstract of all its foreign policy tools, India’s own ability to retain social cohesion while providing economic growth and development will, as Prime Minister Stephen Harper observes, help “lead the world as a whole to greater prosperity and peace”. Indeed, each essay has this very sentiment at its core—the importance of India’s rise for its own people, its region, and indeed as a model for the world in this century.

We hope these essays will provide an intellectual stimulus to debates and discussions that will undoubtedly contribute to shaping our collective future, examine our contemporary challenges and allow us a moment to learn from the journey so far. The world in the 2020s demands more from us. Indians must be ready to deliver.

A decade ago, the Arab Spring levelled the divide — even if briefly — between the Palace and the Street. Powered by social media, the age of digital democracy was upon us. Technology has since become the mainstay of civic activism. Not only are more voices heard, but elected governments are also more responsive to them. And indeed, in many countries, more people are participating in politics than ever before. From attitudes and approaches of platforms and governments to the proliferation of intrusive technologies that invade personal spaces, the gains of the past decade are nevertheless being undermined. The past year or so has made us acutely aware of the weaknesses and threats to digital democracies. Some of these need a coordinated global response.

First, the very platforms that have fuelled calls for accountability often see themselves as above scrutiny, bound not by democratic norms but by bottom lines. The fact is acquisition metrics and market valuations don’t sustain democracy. The contradiction between short-term returns on investment and the long-term health of a digital society is stark. If hate, violence, and falsehoods drive engagement, and, therefore, profits for companies and platforms, our societies are indeed on shaky ground.

To make technology serve democracy, regulation will have to be completely rethought. Big Tech boardrooms must be held to standards of responsible behaviour that match their power to influence and persuade. Moreover, any accountability framework must be global. The global south lives with and depends on technology platforms designed in the north. These platforms have been visibly taken to task by lawmakers and institutions in the countries of their design. Does the larger cohort of users in the developing and emerging democratic world have recourse to such action? And is this denial tenable and fair?

Most democratic constitutions around the world, while protecting expression, do so with safeguards that are meant to secure peace and co-existence in societies that have histories longer and more storied than America’s.

Second, much of Big Tech is designed and anchored in the United States (US). Understandably, it pushes American — or perhaps Californian — free speech absolutism. This is in conflict with laws in most democracies — including in the US after January 6. Most democratic constitutions around the world, while protecting expression, do so with safeguards that are meant to secure peace and co-existence in societies that have histories longer and more storied than America’s.

This American approach to freedom of expression imposed on other democratic societies, at velocities facilitated by technology, is a formula for serious disorder. If American Big Tech wishes to emerge as Global Tech, it must adhere to global democratic norms. Its normative culture must assimilate and reconcile, not prescribe and mandate. In the absence of such an understanding, a clash is but inevitable. It must be emphasised that the fault line would be social norms, not the benefits of technology.

If global democracy and global tech are to coexist, the global south must sit at the high table when regulations are designed and as ethics are embedded in algorithms. Today, the global south’s participation in policy and design decisions that shape our tech future is like the map of vaccinations in our pandemic world — significantly underrepresented in democratic Africa and Asia.

Finally, the greatest danger to the freedom our democracies enjoy is from authoritarian regimes that exploit our liberties and turn them against us. In the real world, Peng Shuai is under house arrest. But in the virtual world, she is presented as being free and happy. Wolf warriors have given a whole new meaning to the phrase “virtual reality”. Recently, an Indian speaker at a transportation conference in China found her microphone turned off because she questioned the Belt and Road Initiative. We are in an unprecedented political landscape where authoritarians weaponise our debates even as we are silenced in theirs. Would any country allow another to open an embassy if it did not have reciprocal rights in the other capital?

The global south’s participation in policy and design decisions that shape our tech future is like the map of vaccinations in our pandemic world — significantly underrepresented in democratic Africa and Asia.

We are living in that perverse reality already. China’s media and government handles conduct aggressive diplomacy in our digital public sphere while we are denied the right to do so in theirs. Beijing and other authoritarian regimes are omnipresent in our digital lives. Their handles bombard us; their chosen narratives besiege and colour the truth. How can we prevent such regimes from gaming the public sphere, and from this perversion of institutions, academia, media, and tech platforms? Their presence on our platforms represents a systemic challenge and a security risk. It must be responded to.

The alleged disruption of America’s elections in 2016 will be child’s play as compared to what may happen in 2024. That year, India, the US and the European Union Parliament will all hold elections — the first such coincidence in the age of digital democracy. We face a perfect storm of misinformation and manipulation. Confronted by wolf warriors, the rest of us can’t be lambs to the slaughter. Open societies have always stoutly defended their borders. Now, they must safeguard these new digital frontlines. At the Summit for Democracy — called by President Joe Biden and addressed by, among others Prime Minister Narendra Modi, it was apparent to all that the democratic world needs to get its house in order. Even as democracies attend to this they need to ensure that other’s don’t burn the house down.

By investing now to build a green, resilient and inclusive economy, countries can turn the challenges of COVID-19 and climate change into opportunities for a more prosperous and stable future.

The decade following the 2009 global financial crisis was characterised by growing structural weaknesses in developing countries, which have been further aggravated by the COVID-19 pandemic and climate change, worsening poverty and inequality. These weaknesses include slowing investment, productivity, employment, and poverty reduction; rising debt; and accelerating destruction of natural capital. The pandemic has already pushed over 100 million more people into extreme poverty and worsened inequality. The effects of climate change are expected to push an estimated additional 130 million people into extreme poverty by 2030.

COVID-19 and climate change have starkly exposed the interdependence between people, the planet, and the economy. All economic activities depend upon ecosystem services, so depleting the natural assets that create these services, eventually worsens economic performance.

The decade following the 2009 global financial crisis was characterised by growing structural weaknesses in developing countries, which have been further aggravated by the COVID-19 pandemic and climate change, worsening poverty and inequality.

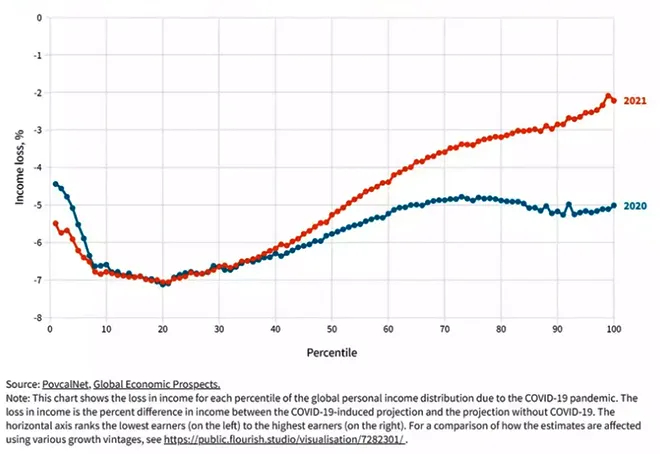

Figure 1: Global income losses due to the COVID-19 pandemic

Image: World Bank

A business-as-usual recovery package that neglects these interlinkages would not adequately address the complex challenges that confront the world nor its structural weaknesses and would likely result in a lost decade of development. Targeting socioeconomic, climate change and biodiversity challenges in isolation is likely to be less effective than a coordinated response to their interacting effects. A continuation of current growth patterns would not address structural economic weaknesses and would erode natural capital and increase risks that affect long run growth. As the depletion of forests, oceans, and other natural assets worsen, the cost of inaction is becoming more expensive than the cost of climate action and it is the poor and vulnerable who are most disadvantaged by it.

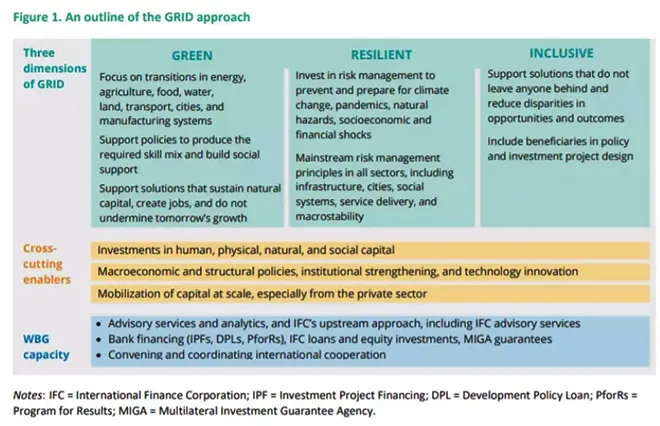

The GRID approach

Image: Worldbank

The solution is to adopt a Green, Resilient and Inclusive Development (GRID) approach that pursues poverty reduction and shared prosperity with a long-term sustainability lens. This approach sets a recovery path that maintains a line of sight to long-term development goals; recognizes the interconnections between people, the planet, and the economy; and tackles risks in an integrated way. Research from the University of Oxford, World Economic Forum and Observer Research Foundation has all shown that a green recovery will not just be beneficial for combating climate change but also offer the best economic returns for government spending and yield development outcomes. The GRID approach is novel in two respects.

First, though development practitioners have long worried about poverty, inequality and climate change, the GRID approach pays particular attention to their interrelationships and thus, on the cross-sectoral nature of critical development policies. Second, achieving GRID implies simultaneously and systematically addressing sustainability, resilience and inclusiveness. GRID is a balanced approach focused on development and sustainability and tailored to each country’s needs and its Nationally Determined Contributions (NDC) objectives. Such a path will achieve lasting economic growth that is shared across the population, providing a robust recovery and restoring momentum on the Sustainable Development Goals (SDGs).

Research from the University of Oxford, World Economic Forum and Observer Research Foundation has all shown that a green recovery will not just be beneficial for combating climate change but also offer the best economic returns for government spending and yield development outcomes.

Recovering from COVID-19 with GRID

The pandemic has inflicted a particularly harsh blow on developing economies. Most urgently, a fast and fair vaccine rollout is critical to an L-shaped recovery. Vaccine access and deployment presents challenges unprecedented in scale, speed and specificities, which will require strong coordination.

Looking ahead, setting a path to GRID will require urgent investments at scale in all forms of capital (human, physical, natural, and social) to address structural weaknesses and promote growth. Special attention is needed on human capital development to rebuild skills and recover pandemic related losses, especially amongst marginalised groups. While the pandemic has amplified the challenges of providing education for all, it has also highlighted how disruptive and transformational technologies can be leveraged in addition to traditional in person learning to help education services withstand the unique pressures of this time.

Recovery packages are an opportunity to prioritise investments in the infrastructure needed to develop and roll out transformative technologies.

Women must be at the center of the GRID agenda as powerful agents of change. Education for girls, together with family planning, reproductive and sexual health, and economic opportunities for women will accelerate the green, resilient and inclusive dimensions of development.

Technology and innovation will play an essential role in promoting low carbon growth. Recovery packages are an opportunity to prioritise investments in the infrastructure needed to develop and roll out transformative technologies.

One takeaway from Glasgow has been that securing green finance at scale will be essential for the GRID agenda. However, developed countries found it difficult to secure the necessary funding for developing countries to implement the green transition to sustainable and equitable development.

But there may be a silver lining. The global economy is awash with excess savings estimated at around $3.9 trillion that are earning negative or low returns and there are $46 trillion of pension funds in search of reasonable returns. The low carbon transition may offer an opportunity for investors, especially as the returns to green investments begin to exceed investments in more conventional technological choices.

Necessity and urgency of systemic investments and transformations

Transformational actions will be needed in key systems — for example, energy, agriculture, food, water, land, cities, transport and manufacturing — that drive the economy and account for over 90 percent of greenhouse gas emissions. Without significant change in these sectors, neither climate change mitigation nor sustained and resilient development are possible. Such a transition, by addressing economic distortions, will promote greater economic efficiency and reduce adverse productivity and health impacts, leading to better development outcomes.

Domestic resource mobilisation can also be increased by enhancing tax progressivity, applying wealth taxation, and eliminating tax avoidance. There is also a need for greater selectivity and efficiency in spending.

But the fruits of the transition may not be evenly distributed and will require a range of social and labour market policies that address adverse impacts, safeguard the vulnerable and deliver a just transition. The GRID approach, therefore, supports a transition to a low carbon economy while considering countries’ energy needs and providing targeted support for the poorest.

Significant reforms of fiscal systems will be needed to mobilise domestic resources and finance the transition. Taxes on externalities are a large and unused source of potential revenue, which can create incentives for the private sector to invest in more sustainable activities. Domestic resource mobilisation can also be increased by enhancing tax progressivity, applying wealth taxation, and eliminating tax avoidance. There is also a need for greater selectivity and efficiency in spending.

A strong private sector involvement will be needed. The scale of investment needed far exceeds the possibilities of the public sector. Reforms are needed to remove constraints to private investment in appropriate sectors and technologies. Thus, at the country level, a strong partnership and dialogue between the public and private sector is urgently needed. And further developing and implementing green financial sector regulation, such as reporting standards and green taxonomies, can help harness investors’ increasing appetite for sustainable investments, which offer both measurable impacts on the environment and society.

However, sustainable and substantial flows of finance across borders will need to supplement domestic efforts. Multilateral development banks (MDBs) and Development Finance Institutions (DFIs) must focus on catalytic and transformational investments in priority areas to develop green, inclusive and resilient project pipelines that support economic growth, and job and income generation. On this front, MDBs can help lower risks for private capital through guarantees and blended finance. But at the end of the day the most effective way to attract private capital is through policies that correct distortions that render environmental destruction profitable.

Multilateral development banks (MDBs) and Development Finance Institutions (DFIs) must focus on catalytic and transformational investments in priority areas to develop green, inclusive and resilient project pipelines that support economic growth, and job and income generation.

Climate change is a reality shaping lives as we speak and not a distant mirage that will materialise only in the future. From Pacific Island nations facing rising sea levels to the Sahel region struggling with longer dry seasons, climate change is changing lives of the poor and vulnerable across the world. The future for the world’s climate vulnerable groups will remain bleak unless we transform policy and economic thinking and secure the financing that is needed.

Countries face a historic opportunity to establish a better way forward. Despite the damage wrought by the pandemic, the exceptional crisis response offers a unique opportunity for a “reset” that addresses past policy deficiencies and chronic investment gaps. Crisis related expenditures can be used to invest in new opportunities, such as accelerating digital development, an expansion of basic service provision, improvements in regional supply chains, strengthening ecosystems services, and policies to catalyze job creation in growth sectors. Private sector dynamism and innovative financing will need to power the recovery and to create economic growth and employment through investment and innovation. Public-private partnerships and key upstream policy reforms can spur private investment (including FDI), support viable firms through restructuring, and enable the financial system to support a robust recovery through the resolution of non performing loans.

As the BRICS passes through a crucial milestone of its existence, celebrating 15 years of its formation, this report examines the initiatives launched since inception and makes recommendations for consolidating and streamlining the agenda.

The BRICS remains a prominent grouping in the global governance architecture due to the individual influence of each member-state and the collective size of their economies. The confidence in BRICS from within and the perceptions outside the grouping are shaped by its successes in institution-building and resource mobilisation. The highlight of BRICS’s success is its strong focus on issues of financial stability and global governance reforms, particularly in areas related to macroeconomic stability. These are supplemented by attention to sustainable development issues backed by finance and technology.

The BRICS agenda has witnessed a steady expansion of its scope ever since its inception. During the initial years, the agenda was focused on responding to the trans-Atlantic financial crisis with a special focus on multilateralism, particularly the need to reform the international monetary and financial architecture. Subsequently, the BRICS established the New Development Bank and the Contingent Reserve Arrangement, two flagship financial initiatives that remain the biggest success stories of the plurilateral to date. Notably, with the outbreak of Covid19 in 2020, there has been a special focus on responding to the pandemic and coordinating recovery.

Given the expanding scope, there is a need for consolidation and streamlining of the BRICS agenda. This will help address structural deficiencies and facilitate the smooth coordination for building consensus on key issues. To realise these goals, a thorough review of the BRICS cooperation mechanisms is necessary. This joint academic study presents an assessment of the various tracks under the BRICS framework, such that the grouping can better pursue the collective agenda of economic cooperation and sustainable development.

The year 2021 has been significant, with the Indian presidency underscoring ‘BRICS@15: Intra-BRICS Cooperation for Continuity, Consolidation and Consensus’ as the theme. The aspect of ‘consolidation’ received special attention. The Indian presidency also helped in concretising several action areas that had remained dormant. A case in point is the Agriculture Research Platform proposed by India at the 2015 Ufa Summit with a memorandum of understanding signed during the Indian presidency in 2016. This was launched in the virtual format in 2021, again during India’s presidency.

India’s presidency of BRICS in 2021 has set a definite example for streamlining of the BRICS agenda. As the agenda consolidates, future presidencies will find room for emerging themes that require urgent attention. Consolidation does not always only mean weeding out weaker sprouts, but to have comprehensive approaches towards setting common goals so that even relatively weaker initiatives can be scaled with resources. A preliminary assessment of the initiatives launched by BRICS is presented in this report.

Progress, as the world has designed and defined it, requires material production which, in turn, requires energy. Historically, therefore, fossil fuels like coal were key in economic growth across geographies. Today, the developed economies stand on the edifice of fossil fuels, carbon-intensive industries, and lifestyles that have resulted in global warming. The same growth path is now being questioned, and the poor and developing countries are being asked to build, find, and fund newer low- and no-carbon models to lift their people out of poverty and achieve their development goals.

As global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

Consequently, there are growing calls for India to declare a net-zero year: To offset its carbon emissions by various processes of GHG absorption and removal. India is aware that such calls are irrational, and despite international pressure, has avoided making pledges or setting hard targets, beyond its commitments at the Paris Climate Conference in 2015. Indeed, “net zero” is not possible with India’s current levels of reliance on coal. Its shift away from this fuel will depend largely on the quantum of additional money and resources that can be invested into alternative energy. However, as global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

In August 2020, UN Secretary-General António Guterres urged India to give up coal immediately. He asked that the country refrain from making any new thermal power investments after 2020, and criticised its decision to hold auctions for 41 coal blocks earlier that year. Similarly, in March this year, in a message to the Powering Past Coal Alliance Summit, the Secretary-General urged all governments to “end the deadly addiction to coal” by cancelling all global coal projects in the pipeline. Pre-pandemic, India had the second largest pipeline of new coal projects in the world. He also called the phasing out of coal from the electricity sector “the single most important step to get in line with the 1.5-degree goal of the Paris Agreement.”

For much of human history, photosynthesis was the primary source of mechanical energy. Human and animal muscles powered by food and fodder, made the world go around. Photosynthesis was also at the root of heat energy derived from burning wood. Eventually, coal replaced wood as the dominant source of heat energy, but still represented the energy of photosynthesis stockpiled over hundreds of years. The advent of the steam engine in the 17th century helped humans change the heat energy released from coal, to mechanical energy.

This development also upended the paradigm of material production. According to a recent estimate, coal was accounting for well over 90 percent of energy consumption in England by the mid-19th century, owing in large part to the steam engine. For long, researchers had been divided over the question of whether coal was pivotal to the industrial revolution. Scholars such as Wrigley (2010) regarded the switch to coal as a “necessary condition for the industrial revolution,” while others like Mokyr (2009) held that the “Industrial Revolution did not absolutely ‘need’ steam…nor was steam power absolutely dependent on coal.”

A November 2020 paper by Fernihough and O’Rourke might just settle the question: Using a database of European cities spanning the centuries from 1300 to 1900, the authors found that those located closer to coal fields were more likely to grow faster. Those cities, the researchers wrote, “located 49 km from the nearest coalfield grew 21.1 percent faster after 1750 than cities located 85 km further away.”

This article explores this line of enquiry by examining the consumption of coal across developed and developing countries, and mapping it against key metrics of energy transition. It finds that countries such as India—with their high dependence on coal and a simultaneous growth spurt in renewables—can be the most effective location for climate finance. This is plausible given that per capita coal consumption in India is still far below that of the developed world, and economic transitions are both inevitable and required to be ‘green’.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-COVID-19 recovery; the same is true for China. Consequently, there is growing scepticism in developed countries, that both India and China will double down on coal and increase production to overcome supply challenges in the future. While such concerns are not unwarranted, they are not unique to the developing world.

To be sure, India is struggling with a coal shortage, which has the potential to derail its post-COVID-19 recovery; the same is true for China.

Germany, for instance, in the first six months of 2021 ramped up its coal-based generation, which contributed 27 percent of the country’s electricity demand. Three factors contributed to this rise: Increase in energy demand amidst the successive waves of the COVID-19 pandemic, increased prices of natural gas, and reduction in electricity generation from renewable energy (particularly wind). Coal is often the bedrock of energy generation, and its use is impacted by complex market processes that cannot be reduced to normative choices.

Energy Use and Coal

Countries of the Organisation for Economic Cooperation and Development (OECD) are using progressively less energy to power their societies. Multiple factors can contribute to this trend, at least in theory. First is the technical improvements in energy efficiency—i.e., the use of less energy to perform the same tasks. Second is the “activity effect”, or the changes in energy use because of changes in economic activity. This would also encompass a “structure effect” which relates to changes in the mix of human activities that are prompted by changes in sectoral activity, such as transportation. And finally, there could be weather-related changes in energy use—for instance, more temperate weather can reduce the need for heating or cooling.

The IEA quantifies these effects, and consistently finds that the reduction in energy consumption in the OECD countries is largely a result of technical improvements in energy efficiency. This means that the reduced use of energy in advanced countries is not on account of any significant changes in consumer behaviour—otherwise, the activity effect would be the primary determinant of the fall in energy use. While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals. Consequently, the Agency has advocated for “urgent action” to counteract the slowing rate of improvement observed since 2015.

While energy efficiency improvements have driven this fall, the IEA finds that the current rate of improvement is not enough to achieve global climate and sustainability goals.

Conversely, developing countries have seen a rapid rise in energy use owing to the activity effect (see Table 1). The increase in economic activity in the developing world is also directly correlated to improvements in life spans and socio-economic progress. While energy use has approximately doubled in countries like India and China from 2005, a large share of global energy efficiency savings is also driven by technical improvements in these countries. However, in the aftermath of the 2008-09 global financial crisis, China implemented a stimulus package that “shifted its manufacturing sector to more energy intensive manufacturing.” A similar trend may emerge in China’s recovery from the pandemic, that may reduce efficiency gains in the future.

It would appear that OECD countries have managed to cut their dependence on coal over the last 15 years quite precipitously. In particular, this seems true of countries like the US and EU members. Japan, meanwhile, is an outlier, having turned to coal to provide base-load power to substitute nuclear energy. In most years between 2005 and 2020, the fall in coal consumption in OECD countries has outpaced the decline in total energy consumption. In 2020, for instance, coal consumption dropped by around 18 percent whereas total energy consumption fell by around 8 percent.

While China has begun to reduce its dependence on coal, it still accounts for the largest share of coal consumption amongst all nations. China is also home to over half of the world’s thermal power plant pipelines—with around 163 GW in pre-construction stage, even discounting the 484GW worth of cancellations since the Conference of Parties at Paris in 2015. China is also one of the last of the biggest providers of public finance for overseas power plants with over 40GW of projects in the pre-construction pipeline.

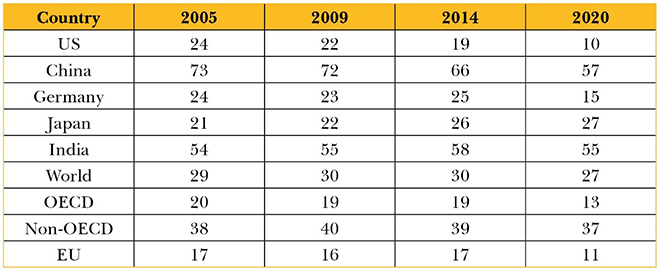

Simultaneously, coal consumption has remained relatively stable at just under 40 percent of primary energy consumption amongst non-OECD nations (see Table 2). In these countries, coal consumption tends to mirror total energy consumption. For instance, in 2018 and 2019, total energy consumption increased by three and two percentage points, respectively. India’s dependence on coal has also remained unvarying. These trends suggest that non-OECD countries such as India require to do much more to contribute to a global reduction in coal consumption and therefore towards net-zero GHG emissions. However, there is more to the OECD’s reduced coal consumption than meets the eye.

Table 2: Share of Coal in Primary Energy Consumption (%)

Country

2005

2009

2014

2020

US

24

22

19

10

China

73

72

66

57

Germany

24

23

25

15

Japan

21

22

26

27

India

54

55

58

55

World

29

30

30

27

OECD

20

19

19

13

Non-OECD

38

40

39

37

EU

17

16

17

11

Source: BP Statistical Review of World Energy, 2021 and author’s own calculations

Since the Earth Summit in 1992, India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions. This approach has often been subject to cross-examination by OECD experts. For instance, in a 2019 report by the Universal Ecological Fund, high-profile experts including a former White House Adviser and a Harvard professor, ranked national climate commitments based on absolute emission curtailment targets. The report clubbed developed and developing countries together in its assessment of the general insufficiency of climate pledges to meet the Paris Agreement’s goal to keep global warming below 1.5 degrees Celsius above pre-industrialisation levels.[1] This should not be a surprise, however, as it is only in consonance with the overall trend of Western academic discourse seeking to dilute the equity principle.

India and other developing nations have argued for an equity-based approach to GHG reduction, commensurate with domestic capabilities and historical emissions.

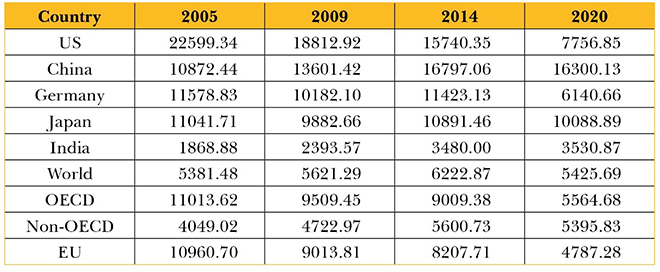

It is a principle that should not be set aside just yet, given the persistent differences in per capita fossil fuel consumption between the developed and developing worlds. Despite near doubling over 2005–2020, India’s per capita coal consumption is still below the global average (see Table 3). The global average, in turn, has remained static around this period because the decrease in the per capita consumption of coal in OECD countries has been partially offset by an increase in the per capita consumption in non-OECD countries. However, the per capita consumption of coal in OECD countries still exceeds that of non-OECD countries, despite much higher levels of wealth and, therefore, capability to transition to renewables and other fuels.

Table 3: Total per capita Coal Consumption (KWh)

Country

2005

2009

2014

2020

US

22599.34

18812.92

15740.35

7756.85

China

10872.44

13601.42

16797.06

16300.13

Germany

11578.83

10182.10

11423.13

6140.66

Japan

11041.71

9882.66

10891.46

10088.89

India

1868.88

2393.57

3480.00

3530.87

World

5381.48

5621.29

6222.87

5425.69

OECD

11013.62

9509.45

9009.38

5564.68

Non-OECD

4049.02

4722.97

5600.73

5395.83

EU

10960.70

9013.81

8207.71

4787.28

Source: BP Statistical Review of World Energy, 2021; World Bank and authors’ own calculations

Indeed, a large share of the decrease in per capita coal consumption in OECD countries is driven by transition to fuels such as natural gas, that are used to generate electricity, particularly in countries like the US. It accounts for around a 34-percent share of primary energy consumption in the US, and 25 percent in the EU, compared to seven percent in India (and a similar share in China). In contrast, the share of gas in India’s energy mix is amongst the lowest in the world. Even as Prime Minister Narendra Modi wants to more than double the contribution of natural gas to 15 percent of India’s energy mix by 2030, the Petroleum Secretary has said that the country cannot rely on natural gas. There are several reasons, including high landed costs relative to coal, complex domestic pricing mechanisms, a lack of pipeline infrastructure and stable supply/ import linkages, and the inability of financially stressed electricity distributors to enter into “take or pay” contracts.

India, therefore, requires relatively greater and more aggressive investments in alternative sources of energy than its developed country counterparts that have had decades to transition to fuels like natural gas. Such financial flows to India can prove to be much more effective vehicles for a net-zero trajectory, compared to similar investments in other parts of the world with higher per capita exposure to coal and relatively slower transition pathways to renewables.

Around 72 percent of India’s GHG emissions are linked to its energy sector. It is clear, that if OECD countries are aiming to accelerate a global reduction in GHG emissions, they will need to help India finance its energy transition and overcome the many resource-linked barriers to the wide-scale adoption of renewables. The high costs associated with renewable energy storage and grid upgrade requirements, are related resource challenges. Since developed countries are unlikely to be satisfied with per capita equity, they would do well to help India hurdle some of its obstacles.

Financing Energy Transition

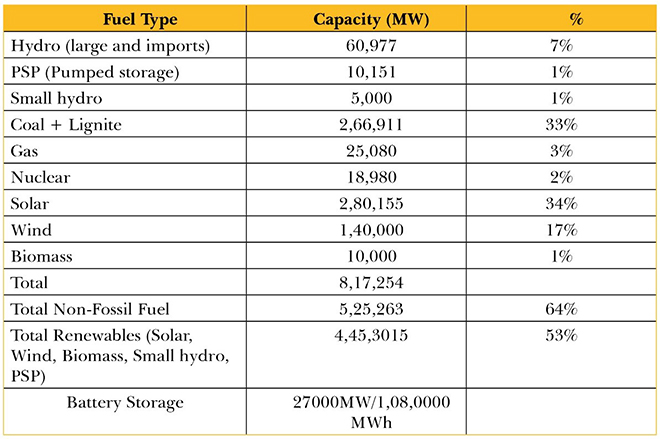

According to India’s Central Electricity Authority’s (CEA) Optimal Generation Capacity Mix, the country’s installed capacity will increase to 817 GW with an additional 27GW of battery storage, by 2029–30 (see Table 4). Of this, firm capacity will contribute approximately 395 GW while renewable sources, around 445 GW. Additionally, a July 2021 study has concluded that more efficient use of existing thermal resources could lead to 50 GW of excess coal capacity with respect to current needs of the system. With limited expectations from nuclear and gas resources and deteriorating coal economics, investments in renewable energy storage options are crucial for managing India’s base load requirements. This requires unlocking of financial and technological flows from the OECD, particularly since there are several uncertainties associated with the cost of battery storage technology. These include risks linked to supply chains and exchange rates.

Total Renewables (Solar, Wind, Biomass, Small hydro, PSP)

4,45,3015

53%

Battery Storage

27000MW/1,08,0000 MWh

Source: Central Electricity Authority; The cost trajectory for battery energy storage system is assumed to be reducing uniformly from 7 Cr in 2021-22 to 4.3 Cr (with basic battery cost of US $75/kWh) in 2029-30 for a four-hour battery system

The technologies that will pave the way to such low-coal path are developing rapidly, with significant progress in renewables, battery storage, and green hydrogen, amongst others. They each require, however, large financial outlays. Moreover, India is still highly dependent on expensive bank lending, which is now hitting sectoral exposure limits, whereas long-term capital is required to finance energy infrastructure. As of April 2020, the exposure of banks and non-bank financial institutions to India’s power sector was already around US$ 160 billion, roughly the lending necessary to finance the country’s renewable energy targets for 2030.

According to the Government of India’s ‘Energy Compact’ submitted to the UN in September 2021, the country required a total investment of US $221 billion to set up 450 GW renewable generation capacity, including associated transmission and storage systems. However, other research has pegged this investment much higher at US $661 billion, to build both renewable energy systems and transmission and distribution systems. The IEA also estimates that India requires a total investment of US $1.4 trillion for clean technologies to help achieve a sustainable development path till 2040. In comparison, developed countries managed a transition away from coal over a longer period of time and with different costs. Investments for clean energy in the Global South needs to be consistently and significantly higher to help achieve the simultaneous goals of SDG 7 (Affordable and Clean Energy) and other development targets.

Advanced countries would do well to recognise that long-term institutional capital is urgently required to help India transition from coal to renewables at scale. What is needed is far more than lip service; nor will change happen only through negotiations at Glasgow at the COP26. Overall, mainstream sources of international climate finance such as the Green Climate Fund and the Global Environment Facility have managed to provide just over a billion dollars in finance for national projects. While there is enthusiasm around green bond financing, the absolute value of issuances towards relevant segments such as renewable energy, is still relatively low at around US $11.2 billion since 2014. To put it in context, the global issuance of green bonds totalled over US $305 billion in 2020 alone, specifically for climate-related and sustainability projects.

India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

A high sensitivity to the cost of capital means that other sources of institutional capital are needed to fill the gap, even as the Indian private sector learns to raise green bonds and co-develops green taxonomies with relevant parties. Most OECD financing towards renewables in developing countries is conducted through debt instruments. According to the International Renewable Energy Agency, cumulative transactions and financial flows from the OECD countries towards renewables development in the rest of the world reached US $253 billion between 2009–2019, of which around US $228 billion was in the form of debt. India accounted for just under US $11 billion of the amount, which is less than 5 percent of the cumulative debt finance by OECD countries.

Table: Cumulative Transactions by OECD Countries into Renewables (2009-2019, %)

Debt

90

Grants

5

Equity and Shares in Collectives

4

Guarantees and Others

1

Source: International Renewable Energy Agency

OECD members must aim to redirect institutional investments towards India. For instance, their sovereign funds and pension funds must adjust to new business models around energy storage and distribution. There are also many possible designs of new financial instruments that could be explored. These could recognise the different capacities and capabilities in developing countries at the outset. For instance, grants and debt funding could be combined in multiple ways to subsidise loans. The scale of grant involvement could be directly proportionate to relevant environmental, social and governance factors, and therefore could incentivise more aggressive low-carbon paths. Similarly, new kinds of investment management and rating modalities could be employed to scale up investments where they are most required to offset planetary risks. The availability of innovative long-term finance for India is critical to any meaningful realisation of global net-zero ambitions. India, for its part, must bite the bullet on large-scale power sector reforms, to improve distributional efficiencies and facilitate inward financial and technological flows.

Conclusion

India’s current per capita coal consumption is three-fifths that of the OECD average, and one-fifth that of China’s. This low per-capita coal consumption in a coal-rich country can and must remain the key feature of India’s growth, going forward. This article demonstrates, that for India to keep its coal in the ground, more and better financing is needed.

A market case for a green transition in India already exists. The last few years have demonstrated India’s appetite, amongst the public and the political class, for a move towards cleaner growth. What it requires now is what this essay calls for: A higher flow of capital towards crucial green sectors—in particular, a higher level of foreign capital inflows towards these sectors, and a better texture of such capital, moving towards a more patient and equitable finance.

Progress as the world has designed and defined it requires material production which, in turn, requires energy. Historically, therefore, fossil fuels like coal were key in economic growth across geographies. Today the developed economies stand on the edifice of fossil fuels, carbon-intensive industries and lifestyles that have resulted in global warming. The same growth path is now being questioned, and the poor and developing countries are being asked to build, find and fund newer low- and no-carbon models to lift their people out of poverty and achieve their development goals.

Consequently, there are growing calls for India to declare a net-zero year: to offset its carbon emissions by various processes of GHG absorption and removal. India is aware that such calls are irrational, and despite international pressure, has avoided making pledges or setting hard targets, beyond its commitments at the Paris climate conference in 2015. Indeed, “net zero” is not possible with India’s current levels of reliance on coal. Its shift away from this fuel will depend largely on the quantum of additional money and resources that can be invested into alternative energy. However, as global climate finance has both under-performed and been subject to clever redesignation, countries such as India remain in dire need of green financing.

In August 2020, UN Secretary-General António Guterres urged India to give up coal immediately. He asked that the country refrain from making any new thermal power investments after 2020, and criticised its decision to hold auctions for 41 coal blocks earlier that year. Similarly, in March this year, in a message to the Powering Past Coal Alliance Summit, the Secretary-General urged all governments to “end the deadly addiction to coal” by cancelling all global coal projects in the pipeline.[1] Pre-pandemic, India had the second largest pipeline of new coal projects in the world. He also called the phasing out of coal from the electricity sector “the single most important step to get in line with the 1.5-degree goal of the Paris Agreement.”[2]