- COMMENTARIES

- SEP 26 2020

Geopolitics and investment in emerging markets after COVID19

Getty

As investors ponder the impact of the world’s greatest economic crisis since the Great Depression, emerging markets (EMs) face a swift reversal of fortune. Some of the fastest-growing economies in the world have been brought to a virtual standstill, reeling with the effects of an exogenous shock to demand, a public health emergency, and nascent infrastructure with which to combat the pandemic.

While multilateral development banks and international financial institutions have moved swiftly to address critical funding shortfalls, the COVID-19 pandemic has dealt severe challenges to the EM growth model — and to the livelihoods of people within these countries. As governments in emerging markets and developing economies (EMDEs) have less fiscal space at their disposal — but harbour an ongoing need for spending on relief and stimulus measures — credit downgrades from the ratings agencies may be inevitable.

Yet, even in the wake of downgrades, this juncture of COVID-induced distress might open up a propitious opportunity for international investors and companies to invest in infrastructure in EMDEs. As such, these investors would address existing and future gaps in critical infrastructure, and ideally provide options for a green future. It will also be critical for governments within EMDE countries to align priorities with pools of institutional capital.

In light of the exceptional circumstances of COVID-19, as investors consider their portfolios, investment committees (ICs) will need to approach their geopolitical asset allocation in a creative way. As the clouds and confusion begin to clear with regard to living in a drastically altered landscape, a significant opportunity is likely to emerge for infrastructure investors to deploy capital to EMDEs with a long horizon.

With $13.7 trillion worth of negative yielding assets held in portfolios, the hunt for yield and long-term value are likely to reemerge as the concerns for safe havens begin to wane. As such, we explore potential guiding mechanisms for investors to help navigate the shifting macroeconomic and geopolitical environment in EMs, as well as potential policy recommendations for officials tasked with rebuilding their countries after the virus.

Macroeconomic snapshot: the perfect storm

Emerging markets and developing economies have faced a perfect storm in the wake of COVID-19. As the virus hit China in January 2020, emerging markets faced unprecedented capital outflows from foreign investors – dwarfing outflows during previous crises, including the 2008 Financial Crisis (GFC), the taper tantrum of 2013 (when investor panic triggered a spike in US Treasury yields on news that the Federal Reserve was slowly putting the breaks on its quantitative easing programme), and the renminbi depreciation of 2015. In the face of outflows – and depreciation of local currencies – sovereign borrowing costs have risen, thus placing a strain on the ability of many EMDE governments to continue to fight the public health emergency, as well as to shore up their economies amidst the reverberating shock to demand.

As a result of the sudden economic stops around the globe and the ongoing lockdowns, trade activity has plummeted. Commodity prices – typically a bellwether for economic growth for many EMDEs – have remained painfully low, with the price of West Texas Intermediate crude oil plunging to an unprecedented nadir in negative territory. Demand for tourism – another key driver of economic growth and job creation in many emerging economies, such as Mexico, the Philippines and Thailand – remains severely curtailed. Indeed, international tourist arrivals are projected to plunge by some 60 to 80% in 2020. Remittances – another key source of national income and contribution to household purchasing power for many EMDEs – are down, and this precipitous fall is currently most pronounced in Latin America.

And, while many companies rush to secure funding from governments and capital markets, non-financial corporations in EMs continue to suffer from a debt overhang. Some $31.2 trillion sits on non-bank corporate balance sheets. At the end of 2019, an estimated $3.8 trillion of this debt was denominated in US dollars, which might place undue pressure on borrowers to service their debt in light of local currency depreciation. (If one accounts for offshore borrowing and the use of FX derivatives, the total amount of US dollar denominated debt on EM corporate balance sheets could be much higher). Looking at total debt spread across corporates, banks and sovereigns, some $7 trillion of bonds and loans are due to come to maturity in EMs through the end of 2021.

The upside: amplified macroprudential measures

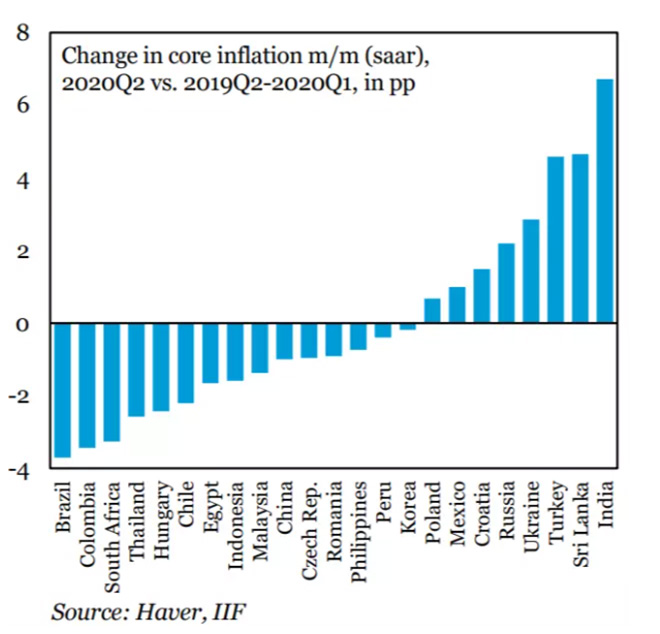

Despite this conflagration of economic challenges, governments and central banks within some EMDEs continue to exhibit a strong implementation of macroprudential policies – namely, by working to keep a lid on inflation, reducing the fiscal deficit and maintaining floating exchange rates. Core inflation (omitting volatile food and energy prices) remains muted within many EMDEs, underscoring the ability of central banks and economic officials to maintain successful inflation targeting regimes, both prior to and throughout the corona crisis. Notable examples on this front include Brazil, Colombia, Vietnam and the Philippines.

Additionally, at the end of 2019, as a result of concerted efforts to reduce their fiscal deficits, Colombia posted the first fiscal primary surplus in almost a decade and Brazil posted its smallest annual fiscal deficit since 2014. As a result of lockdowns and recessions, imports have also been constrained: consequently, several countries boast current account surpluses. Notably, Brazil’s trade gap has narrowed by the greatest amount since 2007. And, although EM currencies were battered throughout the start of COVID-19, depreciation against the US dollar has largely stabilized, with some currencies significantly undervalued at the time of writing.

On the whole, central banks in EMs have been able to step in and help provide liquidity support to households and corporations hard hit by the crisis. In many cases, central banks have used the architecture and tools established during the GFC to be able to help to enable price stability and sufficient liquidity and functioning of financial markets. One EM central bank has even embarked upon the policy experiment of monetary financing; that is, of monetizing state debt by buying bonds directly from the government, rather than from the secondary market.

While foreign investors digest these moves, it is important to point out that at the time of writing, governments and central banks – acting in concert with the financial sector and central banks in advanced economies – have thus far been able to avert a financial crisis, despite the onset of a global health emergency and the worst peacetime economic slowdown since the Great Depression. While many EMDEs take up the fight against COVID-19 and its aftermath – mirroring actions and commitments from officials in advanced economies to “do whatever it takes” – EMDEs do indeed have less fiscal room for manoeuvre than developed markets.

To date, the COVID-19 fiscal response in EMs has amounted to only one-fifth of that of advanced economies. In contrast, countries such as the US can reap more fiscal space by being the world’s reserve currency. Additionally, some eurozone bonds (such as the German 10-year bund) are also considered to be a safe haven for some institutional investors.

Amidst mounting sovereign debt and constrained fiscal space, credit downgrades in EMs have begun to unfurl, posing a challenge to the ways in which investment committees traditionally approach geographical asset allocation. In the wake of a downgrade, it is important for investors to take a step back and ask the following questions:

- Which countries demonstrated a robust commitment to implementing macroprudential measures prior to the outbreak of COVID-19?

- Which countries have a strong domestic market, rendering them somewhat resilient in the face of an exogenous shock?

- Which countries have boasted strong labour force productivity, with a commitment to boost competition in sectors of long-term demand in the post-COVID recovery landscape?

Even if a country receives a downgrade as a result of its enhanced fiscal efforts deployed to help combat COVID-19 and to address the exogenous shock of the pandemic, it is important to recognize that for some countries, these efforts are an expansion of spending during exceptional circumstances, rather than a departure from an overall commitment to macroprudential measures.

Reading the tea leaves: geopolitics and deploying long-term capital to infrastructure

While we might recognize that there are some countries that fit the bill in terms of their economic planning and policy, for investors looking to EMDEs, geopolitics can often cloud the landscape for investing. For the private sector, and specifically investors and executives, geopolitics relates to infrastructure in three key ways:

1) Geopolitical asset allocation, at the portfolio level

On a country-by-country basis, which countries manifest the strongest risk-reward ratios? Here, it is important for investors to distinguish between absolute and perceived risk. For example, an institutional investor with little risk appetite might consider investing in airports in Paris to be a geopolitically low-risk investment, versus deploying capital to airports in Vietnam, which might be perceived as higher risk. However, in light of the rise of populism in advanced economies, and risks of potential nationalization, some countries or regions perceived to be less geopolitically risky might indeed harbour more absolute risk.

2) Managing geopolitical risk, at the asset management level

While operating assets on the ground, infrastructure investors are often confronted with effectively managing geopolitical risk at the asset level. Several questions that may need to be addressed include: how might any (small or large) breach of project safety engender a shift in perception by the host country, potentially rendering the investor a target of local political ire? How might changes in the regulatory environment affect investments, and how might investors anticipate potential changes in the regulatory environment? How might investors best navigate potentially conflicting positions between federal, provincial and municipal authorities? Recognizing that taxes can become a tool amidst a rise in geopolitical tensions, how might investors be able to anticipate potential changes in taxation that might hinder their position, both in terms of profits and also in ease of operation?

3) The intersection between geopolitics and economics

Infrastructure investing has the power to spur a positive feedback loop within an economy. By creating both direct and indirect economic growth and employment, and improving livelihoods and quality of life, greenfield infrastructure investments can provide a foundation for generating economic growth via agriculture, manufacturing and service activity. Brownfield infrastructure investments – including upgrades to existing assets – have the potential to greatly enhance the quality of life in a given area, as well as to boost efficiency (for example, upgrading a toll road can ease traffic and congestion). By acting as a foundation and a multiplier effect of economic growth and quality of life, infrastructure investments can, over time, potentially reduce geopolitical risk by contributing to livelihoods and generating economic opportunities.

In trying to discern which EMDE countries may prove attractive for investment, it is advisable for investors to identify which governments exhibit a strong capacity for follow-through on policy reform. In order to attract voters – or possibly, foreign investors – political leaders might promise many pro-growth or pro-business policies. To promise is, of course, not enough. The question for investors is: which countries have demonstrated the potential to ratify and implement such change?

For example, the Brazilian Congress ratified the country’s historic pension reform in October 2019. Although this had been a policy priority of the current and previous presidential administrations, the country’s legislative body followed through on the reform. In the case of India, while many executives and investors had complained about the opacity of the country’s complex tax system, the implementation of the goods and services tax (GST) greatly simplified taxation. Sometimes, policies such as the GST might induce short-term pain for long-term gain. For investors, It is advisable to identify signs from governments which might harbour this long-term vision – and the capacity to see it through to implementation.

For investors, it is advisable to identify signs from governments which might harbour this long-term vision — and the capacity to see it through to implementation. Partly, this depends upon the strength of existing institutions, as well as the ability to reform institutions as the need arises. Notably, in the case of Brazil, while some investors have been deterred from the ongoing Lava Jato investigations, this demonstrates the strength of the institution of justice.

Crucially, it is not necessarily only democracies which exhibit the capacity for follow-through on pro-business and growth-oriented policy reforms, as well as the ability to constructively reform institutions. Vietnam is a key example here, where foreign and institutional investors continue to respond positively to the government’s ongoing market reforms by deploying billions of dollars to the country. Again, taken together with a consideration of which governments might harbour a commitment to macroprudential measures, a tried-and-tested capability for follow-through on policy reform may also be a signpost for investment committees to identify in light of a potential downgrade.

At the sector level: building back green

In the World Economic Forum’s Great Reset initiative, as many governments chart out policies to constructively rebuild their countries in the aftermath of COVID-19, a clear emphasis is placed on addressing critical gaps in soft infrastructure, which may help enable countries to withstand a health crisis or a sudden stop in economic activity. This includes hospitals and public health institutions, broadband connectivity, educational platforms to continue teaching in a virtual classroom, and supporting sustainable food security, access to clean water and personal protective equipment (PPE).

Of course, these investments are not limited to EMDEs. Advanced economies such as the US and France have worked to address some of these gaps in critical infrastructure in the wake of the pandemic. Accordingly, these types of soft infrastructure categories – rather than the hard infrastructure of ports, roads, airports and bridges – are likely to be immediate policy priorities for some EMDEs in magnetizing foreign investment. Utilities and power are also likely to rank high on the list, insofar as power underpins this softer infrastructure.

In considering economic vitality after COVID-19 – and to do so in a way that shapes a more sustainable and resilient future – governments across the globe have touted green and digital as key policy priorities. However, in order to attract foreign investment, EMDEs will need both strong institutions, as well as the capacity for institutional reform, which would possibly then foster a sense of confidence in fund managers that these might be deployed effectively.

Environmental, social and governance (ESG) indices have outperformed traditional benchmarks during the current pandemic and are likely to attract more funds going forward. Nevertheless, it is crucial for ESG investors to identify jurisdictions with clear green taxonomies and government policies designed to enhance innovation and market creation.

Government action, alone, can’t do the job: the private sector will have to be the locus of climate action. This should require a fresh focus on the ease of doing business, policy certainty and a regulatory landscape, which prioritizes green sectors. Undoubtedly, for many companies facing high fixed costs and negative sales – as well as heightened uncertainty about the future – the coronavirus pandemic has constrained the ability for some corporations to deliver on past commitments to consume green energy.

A critical question to address in the post-pandemic era will be the creation of new growth centres and adaptations of growth models. In EMDEs, cities have been the locus of economic activity and have successfully brought millions out of poverty. However, as the current pandemic – or recent waves of natural disasters – show, one shock can risk undoing the work of years and potentially push millions back into poverty. Highly dense urban centres can also put pressure on both the environment and natural resources. As the risks of climate change mount, growth models in emerging markets should need to prioritize resilience and quality of life, alongside efficiency and profits. This can include the rapid development of smart cities, something Singapore has done remarkably well.

Additionally, while parts of global value chains might be onshored in the wake of COVID-19, a potentially significant opportunity arises for international investors to deploy capital for localizing supply chains. A well-developed domestic supply chain may require improved connectivity, both physical and digital. Digital platforms and knowledge sharing will likely be integrated nodes on the value chain. Smaller self-contained habitats will be required for workers, and sustainable solutions are likely to be needed for housing, mobility and utilities, as well as natural resource management.

Investments in clean power should be requisite to underpin both old and new economic growth: that is, for industrial activity and digital connectivity. Finally, these countries will need to develop the human capital required to carry out jobs that are likely to rely upon increasingly complex technologies. Catalyzing infrastructure investment in the wake of COVID might provide much-needed jobs, and may also sow the seeds for future skills to meet changing patterns of demand in the new economy.

Conclusion: getting it right

In the pre-COVID age, one advanced economy within the Asia-Pacific region has managed to deftly invest in infrastructure in developing countries for the long haul: Japan. Indeed, Japan has had a long history of exchanging overseas development assistance for resources to fuel its manufacturing growth. In later years, it has become an exporter of what Prime Minister Shinzo Abe calls “quality infrastructure investment”.

Recipient countries such as India have affirmed the high quality of such investments – including bullet trains and subway stations – and the Japanese government has also prioritized the facilitation of knowledge exchanges to help nurture and develop human capital. Critically, Japanese infrastructure investment is not necessarily hinged upon whether a country is classified as a democracy, suggesting that both lucrative profits and economic and financial stability may not just emanate from states which profess to be democratic.

It should be noted that Japan has been criticized for its use of coal at home and for its development of coal plants abroad. Indeed, even in light of commitments made by several Asian governments (most notably, South Korea) to “build back green”, Japan has allocated only a nominal amount of the country’s $2.1 trillion COVID relief package toward the green energy transition. However, as relief segues into stimulus and the global economy inches toward recovery in a post-pandemic world, Japan has the potential to help provide an environmental component with its quality infrastructure investments. Indeed, Environmental Minister Shinjiro Koizumi recently announced increasing regulation for building coal power plants overseas — a move that is in keeping with the Japanese business community’s action to help reduce carbon emissions.

Similarly, Australia has declared its intention to become a “renewable energy export superpower” with a commitment to export solar energy to Singapore via cables and the use of the world’s largest battery. A resource-rich country known for exporting coal and natural gas around the world, Australia has the potential to build upon its past relationships and know-how to help bolster the energy transition within emerging markets and advanced economies alike.

In a world of competing visions within foreign policy, both Japan and Australia demonstrate that it is possible to invest abroad without ideology and preconditions – which is a straightforward approach, and likely necessary to help address infrastructure gaps around the globe.

Finally, while infrastructure investors can look to generate profit in EMDEs over the long term, it is advisable for the governments within these countries to explain to their voting publics the importance of attracting foreign capital. This requires clear data, and also versatility in how this data and story is communicated to different interest groups – be it provincial or municipal governments, citizens or local businesses. The story needs to continue throughout the lifespan of such investments – and indeed, potentially after completion.

Development banks within host countries can help provide such continuity amidst changes in administration at the federal level. It is also worth exploring the ways in which some development banks can become independent entities, rather than organized via political appointments. This might provide a much-needed ballast for the dry powder that waits in the wings – and for institutional capital with nascent exposure to infrastructure in emerging markets.

This commentary originally appeared in World Economic Forum.